German IFO Survey Continues to Weaken

Overview IFO climate, current conditions, and expectations all slipped to lower readings in August compared to their levels in July. The rankings of the August indexes for climate, current conditions, and expectations are all extremely weak. The climate index has a 7.5 percentile standing, current conditions have a 14.3 percentile standing, and expectations have a 5.4 percentile standing. Over the last four months, there has been a cumulative drop in the diffusion gauges of 20 points for climate, 14.1 points for current conditions, and 19.8 points for expectations.

Climate Climate rankings by sector show the highest standing for construction at a 31.8 percentile standing compared to the lower 6.8 percentile standing for services. None of the sectors displays a climate reading above the 50% mark that designates, in each case, the median for the sector. Climate changes are negative in each of the last four months across all sectors. Wholesaling and retailing are weaker month-to-month for five straight months.

Current Conditions Current conditions erode and erode significantly in each sector compared to July. The current business situation shows declines across each of the last five months for the headline as well as in manufacturing, construction, and wholesaling. Retailing and services have shown month-to-month declines in four of the last five months. Construction actually has declined for six months in a row. Over the last 14 months, manufacturing, construction and wholesaling have seen diffusion fall month-to-month in 11 of those 14 instances. Retailing and services have declined in 8 of those 14 instances. There has clearly been an intense period of weakness over the past five months, there was some respite 6 to 9 months ago, and then 10 to 14 months ago, there was a previous heavy menu of persistent month-to-month declines. The current period represents another significant step down in current activity.

Expectations Expectations weakened in August compared to July for overall expectations as well as all sectors except retailing. Month-to-month expectations have weakened for four months in a row for overall expectations, manufacturing and construction. Expectations have weakened for three of four months in wholesaling and service and in two of four months in retailing. Expectations also have been through cold, warm, cold cycling phases with sectors generally showing persistent declines from September 2022 to March 2022, improving more persistently form December 2022 to April 2023, and then eroding consistently over the last four months.

Summing up These patterns for expectations are interesting in part because the readings continue to hug to very low standings. Since March 2022, expectations have ranged between a high rank standing of 17.4% and a low of 1.8% (in July 2022). Currently, that standing is still very weak at 5.4%. German expectations have been nailed to the floor and unable to sustain a recovery for quite a while.

The IFO survey presents a sour look of the Germany economy - not only with the low rankings of the various metrics and the consistency of weakness across the measures and sectors but also because those same traits largely apply to momentum which is broadly experienced and has tuned more decidedly negative again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Mar 19 2026

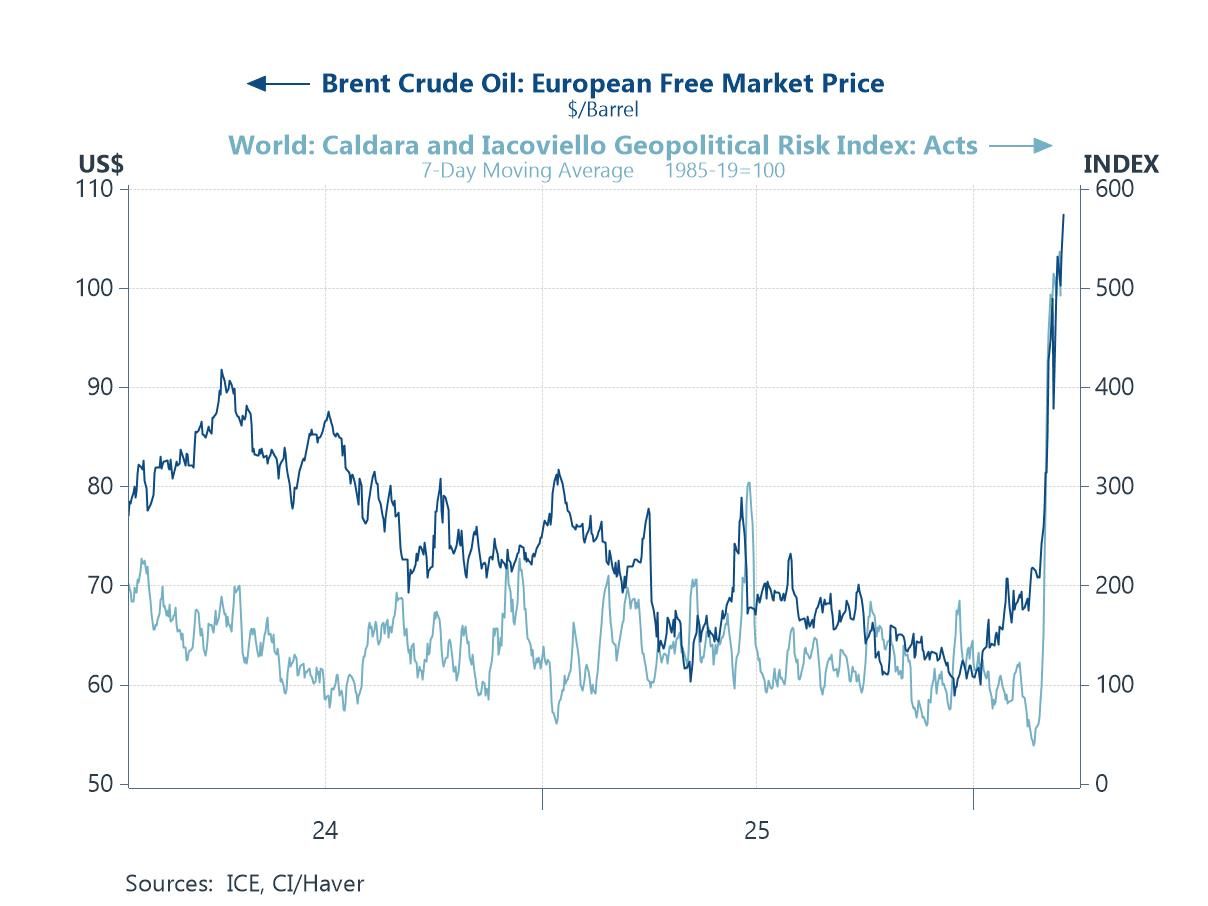

Global| Mar 19 2026Charts of the Week: Energy Shock — Early Signals, Uncertain Fallout

by:Andrew Cates