U.S. Existing Home Sales Fall Sharply in October

by:Tom Moeller

|in:Economy in Brief

Summary

- Sales weaken to 13-year low.

- Home prices slip again.

- Purchases decline in most regions of country.

Sales of existing homes declined 4.1% (-14.6% y/y) during October to 3.79 million (SAAR) after falling 2.2% to a little-revised 3.95 million in September. Sales stood at the lowest level since August 2010 after the most recent peak of 6.56 million in January 2021. The sales figures are based on closings of sales signed in earlier months. The Action Economics Forecast Survey expected October sales of 3.90 million units.

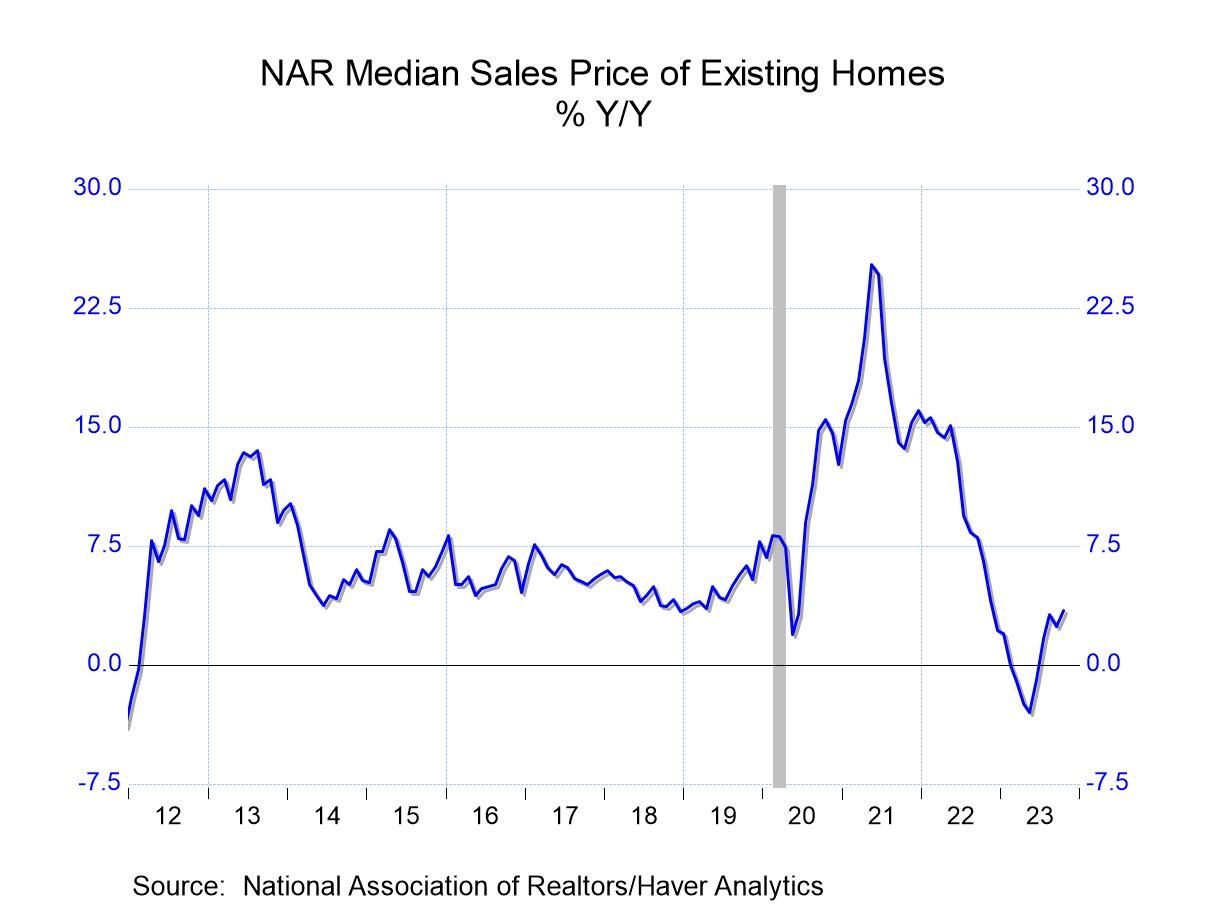

The median price of an existing home (NSA) eased 0.3% (+3.4% y/y) to $391,800, the fourth consecutive month of price decline. Prices were 5.3% below the June 2022 peak of $413,800. The median price of an existing single-family home also slipped 0.3% (+3.0% y/y) to $396,100 after falling 3.1% in September. The median price for condo & co-ops gained 0.6% (7.6%) to $356,000 after easing 0.1% in September.

Single-family home sales fell 4.2% (-14.6 y/y) to 3.38 million units after falling 1.9% in September. Sales remained 42.2% lower than the high of 5.85 million in October 2020. Condo and co-op sales fell 2.4% (-14.6% y/y) to 410,000 after weakening 4.5% in September. Sales have fallen 45.3% from their January 2021 high of 750,000.

Overall sales were mixed m/m across the country. Sales in the Northeast fell 4.0% (-15.8% y/y) to 480,000 last month after rising 4.2% in September. Sales in the Midwest held steady in October (-13.9% y/y) at 930,000 after falling 4.1% in the prior month. Sales in the South fell 7.1% (-14.6% y/y) to 1.69 million, the seventh decline in eight months. Sales in the West declined 1.4% (-14.8% y/y) to 690,000 after falling 6.7% in September.

The number of existing homes for sale (NSA) rose 1.8% (-5.7% y/y) to 1.15 million in October after increasing 2.7% in September. The supply of homes on the market at the current selling rate (NSA) edged up to 3.6 months from 3.4 months, the largest supply since June 2020. The record low in supply of 1.6 months was reached in January, 2022. These figures date back to January 1999.

The data on existing home sales, prices and affordability are compiled by the National Association of Realtors. The data on single-family home sales extend back to February 1968. Total sales and price data and regional sales can be found in Haver's USECON database. Regional price and affordability data and national inventory data are available in the REALTOR database. The expectations figure is from the Action Economics Forecast Survey, reported in the AS1REPNA database.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates