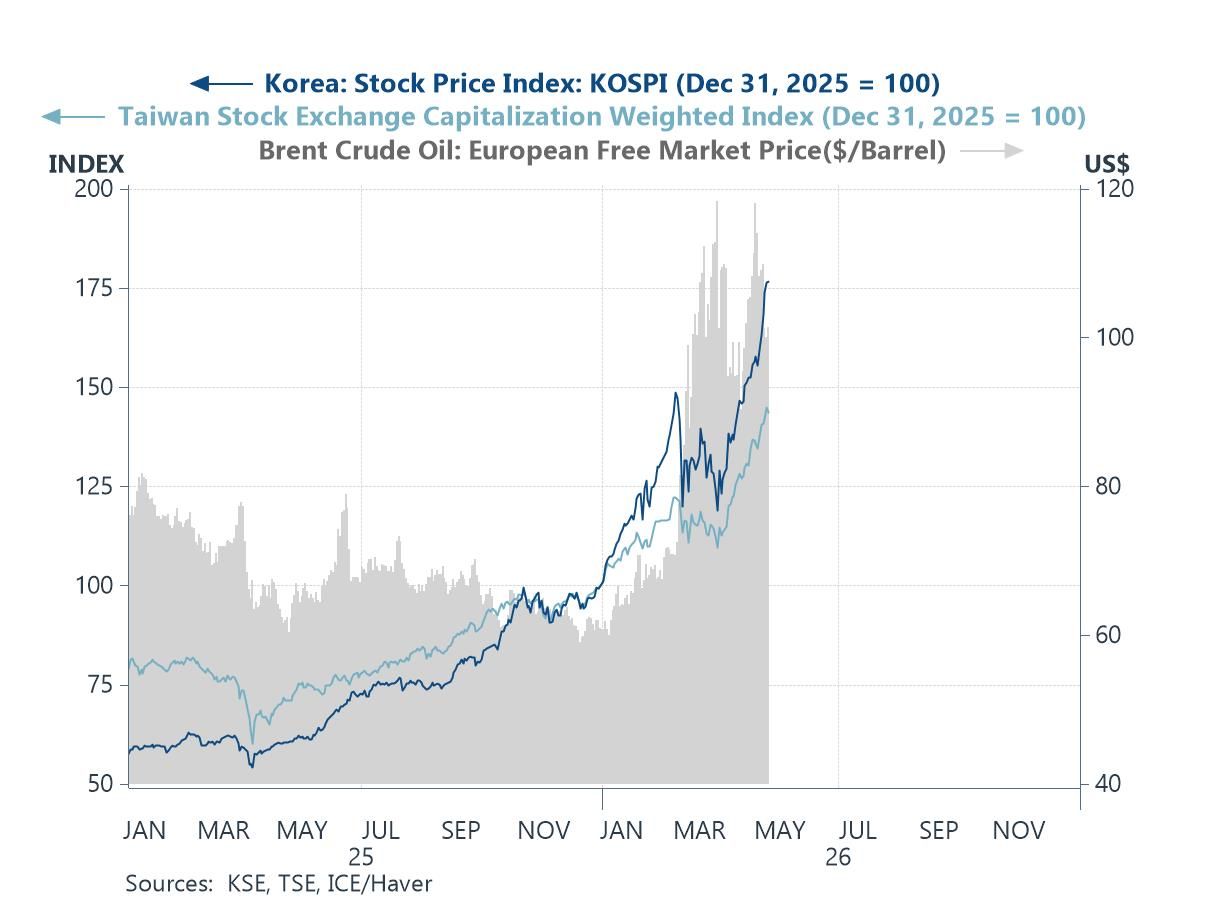

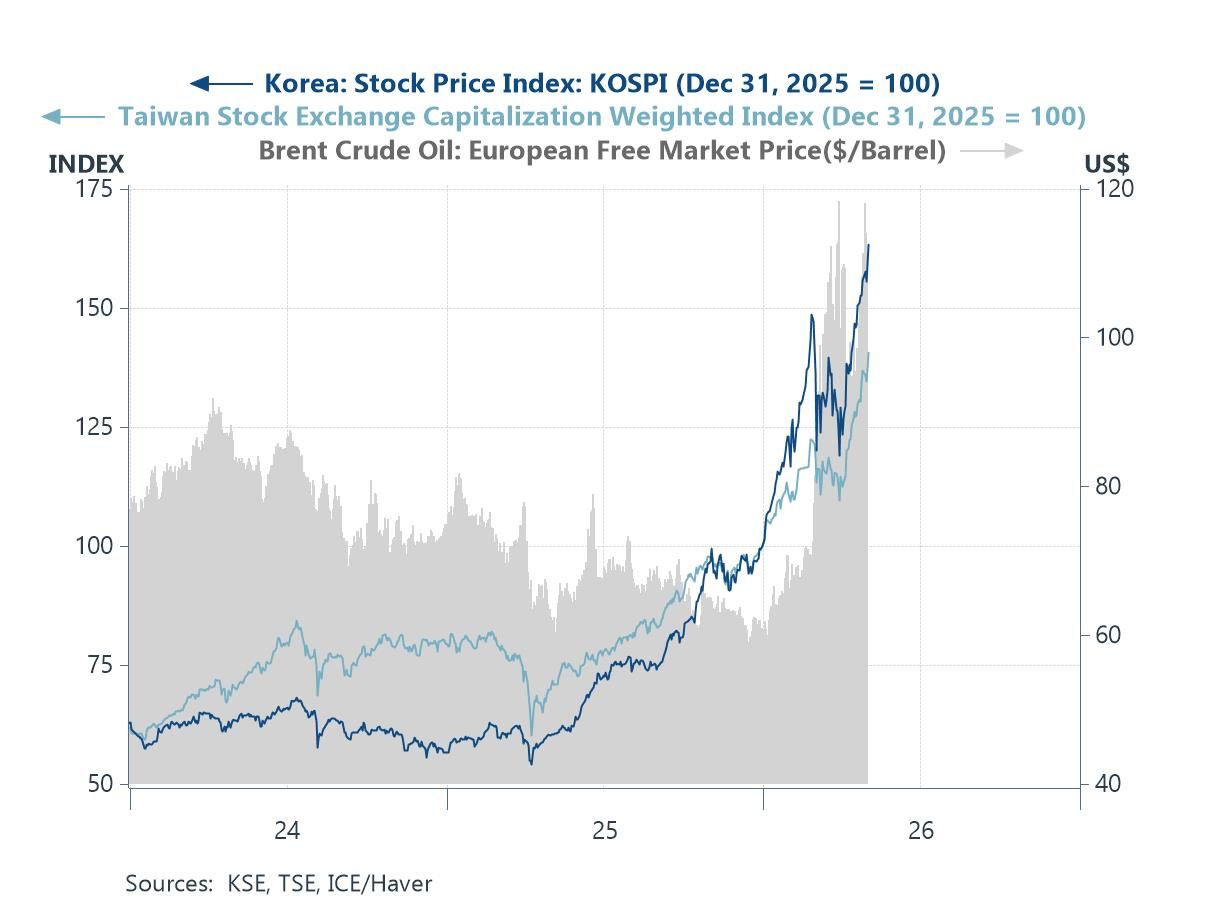

Asia

AsiaIn this week's Letter, we trace three threats converging on Asia's inflation outlook. The first is renewed US tariffs, with the latest salvo of duties imposed over alleged forced labour issues. That move is widely seen as a replacement for the now-expired Section 122 tariffs, with only mild incremental effects from the new Section 301 duties. Set against that, the US effective tariff rate has pulled back from its 2025 highs in recent months (chart 1). The second is the Strait of Hormuz, where the re-escalation of US-Iran tensions has once again reduced shipping volumes to a trickle. Crude oil prices have been driven up as a result (chart 2). It could have been worse, were it not for China's sharply reduced crude imports over the period (chart 3). Arguably, though, at least part of that reduced intake simply reflected the absence of supply from the Strait. The third is the ongoing El Niño event, which several authorities have warned will likely be the largest on record (chart 4). It risks disrupting food crop yields, among other effects, channelling a price shock through food supply. Together these pressures threaten to upend the pullback in commodity inflation seen in recent months (chart 5), once again complicating policymaking. As an aside, we also explore economy-specific political developments that are brewing or could become an issue further down the road. One is the recent resignation of Indonesia's central bank governor, which came amid protracted rupiah weakness (chart 6) and concerns about fiscal health.

Tariff trouble Recent US forced labour tariffs have revived concerns, pushing the tariff theme back to the fore. The US imposed additional Section 301 duties of 10% or 12.5% on imports from 60 investigated economies, effective 24 July 2026. These followed USTR investigations into those economies' failure to impose and enforce prohibitions on goods produced with forced labour. They took effect the same day the temporary 10% Section 122 global surcharge expired by statute, and are seen as its replacement. Yet overall US effective tariff rates, calculated as duty as a percentage of the respective dutiable value, have pulled back significantly from their 2025 highs (chart 1). That retreat began with the numerous bilateral trade deals the US eventually struck with many of its trading partners. It went further in February, when the Supreme Court struck down President Trump's tariffs imposed under the International Emergency Economic Powers Act (IEEPA). That ruling dented the overall impact of US tariffs on its trading partners, with possible tariff refunds still in the works. Cutting the other way, the Section 122 surcharge had partially raised overall rates while it ran. Even so, some estimates suggest the new duties will only marginally increase US effective tariff rates on its trading partners.