Global| Nov 06 2018

Global| Nov 06 2018German Orders Barely Edge Higher and Rise for Two Consecutive Months

Summary

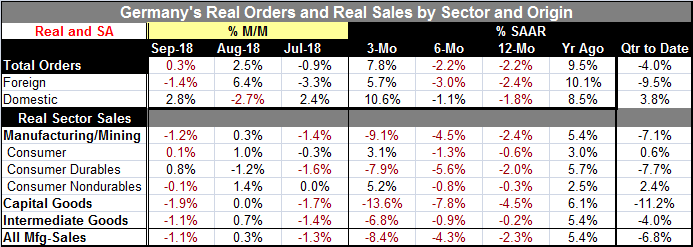

German (real seasonally adjusted) orders rose by 0.3% in September after a 2.5% gain in August. Orders rose for two months in a row for the first time since December when orders completed a run of five consecutive increases. January [...]

German (real seasonally adjusted) orders rose by 0.3% in September after a 2.5% gain in August. Orders rose for two months in a row for the first time since December when orders completed a run of five consecutive increases. January through July of this year, real orders fell in six of seven months until putting together this two-month string of increases.

German (real seasonally adjusted) orders rose by 0.3% in September after a 2.5% gain in August. Orders rose for two months in a row for the first time since December when orders completed a run of five consecutive increases. January through July of this year, real orders fell in six of seven months until putting together this two-month string of increases.

Order trends are still far from solid with declines for overall domestic and foreign orders over 12 months and six months. But there are increases in three-month orders for (1) total orders, (2) domestic orders, and (3) foreign orders. The trifecta of three-month gains is encouraging, but we also know how volatile three-month ‘trends’ can be. Moreover, real sector sales show decline on all horizons for total and manufacturing sales as well as for consumer durables, capital goods and intermediate goods sales. The exceptions that show a three-month rise and declines on the other horizons are for total consumer goods and nondurable consumer goods. That is very thin gruel for ‘good’ news.

Sales and order trends for German firms remain on uneven ground. Domestic orders increased by 2.8% and foreign orders decreased by 1.4% in September 2018 on the previous month. New orders from the euro area were up 2.4%, while new orders from other countries decreased 3.7% compared to last month. Germany is basing its recovery on sales executed either at home or elsewhere inside the euro area. Right now that is looking like a threatened base.

The quarter-to-data calculations (which now are for a completed Q3) echo all the same trends but with total orders falling in Q3 with foreign orders lower on balance and only domestic orders higher. Total real sector sales are lower as are manufacturing sales in Q3. In addition, capital goods and intermediate goods sales are lower in addition to sales of consumer durables. Rising in Q3 are overall consumer sales and sales of consumer nondurables- a familiar theme.

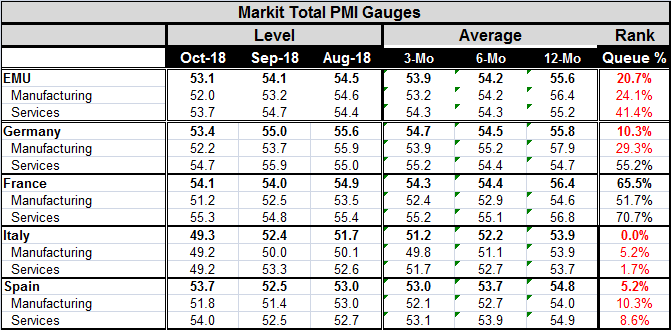

The German order statistics from EMU members which are for September are curiously strong showing orders up 2.4% in the euro area at a time when euro area growth is faltering. In October, the euro area composite index is at a 20.7 percentile standing, indicating that it has been weaker only a bit more than 20% of the time since January 2014. The German composite PMI itself has been weaker on this time line only about 10% of the time. France’s performance has gone moderately well on a fringe manufacturing reading and a firmer service sector performance. But both Italy and Spain are showing abject weakness with 10th percentile or lower queue standings for their composites and sectors on what clearly are low diffusion readings. Italy shows raw diffusion scores for its composite, manufacturing sector and service sector that all demonstrate contraction.

In this environment, it is a bit harder to interpret the recent firming in German orders as the start of positive news that will have legs, especially with its reliance on a good performance on transactions within a weakening euro area.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief