Global| Oct 21 2015

Global| Oct 21 2015Japan's Exports and Imports Lose Momentum

Summary

Japan's goods exports and imports fell in September with imports falling faster thereby shrinking the trade deficit. Export trends show nominal exports weak on all horizons of one year and less, and declining on balance over six [...]

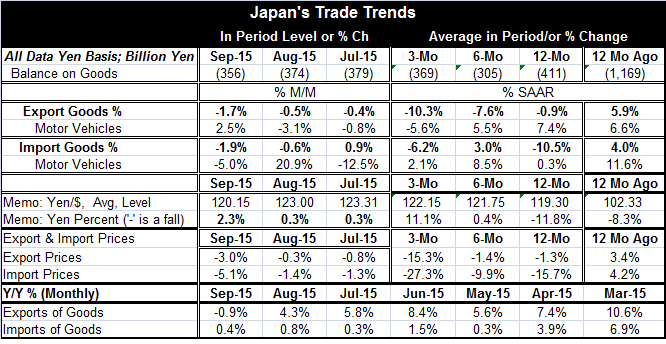

Japan's goods exports and imports fell in September with imports falling faster thereby shrinking the trade deficit. Export trends show nominal exports weak on all horizons of one year and less, and declining on balance over six months and three months. Nominal imports have a different pattern but are substantially lower over 12 months and over three months.

Japan's goods exports and imports fell in September with imports falling faster thereby shrinking the trade deficit. Export trends show nominal exports weak on all horizons of one year and less, and declining on balance over six months and three months. Nominal imports have a different pattern but are substantially lower over 12 months and over three months.

On the export side, motor vehicle exports have been slowing and adding in to the trend of export weakness. On the import side, vehicles have showed an erratic pace but one that has consistently positive boosting imports thereby working against their overall trend weakness.

Over the past year, the yen has been more or less steady.

Export and import prices have be steadily falling over the past year. Import prices have been dropping more substantially largely because of the role of weak global oil and commodity prices. Thus, some of the flow weakness is nominal. Weak export and import trends show price effects along with volume effects. However, even inflation-adjusted export trends appear to be weak. Import trends are stronger after adjustment.

Japan needs some help from its international trade side to gain economic traction. Today

Japan's all-sector industry index fell and it has been lethargic for a long time. Monetary stimulus per se can only do so much. Perhaps the most potent channel for that stimulus was through the foreign exchange rate and now that impact seems to have died out. Japan's domestic demand is certainly not self-starting. Monetary stimulus seems to be losing its edge. And now Japan may be in risk of losing its international life line to growth as export growth has gone slack. This is a very worrisome development for Japan, a country that is running out of options.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates