Global| Feb 28 2013

Global| Feb 28 2013Jobs Rise in Germany!

Summary

The chart shows not just a difference between Germany and the rest of EMU (actually the result is for EMU so it has the German result embedded in it, lessening the appearance of the true German/Non-German EMU difference!) Germany and [...]

The chart shows not just a difference between Germany and the rest of EMU (actually the result is for EMU so it has the German result embedded in it, lessening the appearance of the true German/Non-German EMU difference!) Germany and the EMU are not just going at different speeds; they are going in opposite directions.

The chart shows not just a difference between Germany and the rest of EMU (actually the result is for EMU so it has the German result embedded in it, lessening the appearance of the true German/Non-German EMU difference!) Germany and the EMU are not just going at different speeds; they are going in opposite directions.

The German unemployment rate continues to fall while in EMU it continues to rise.

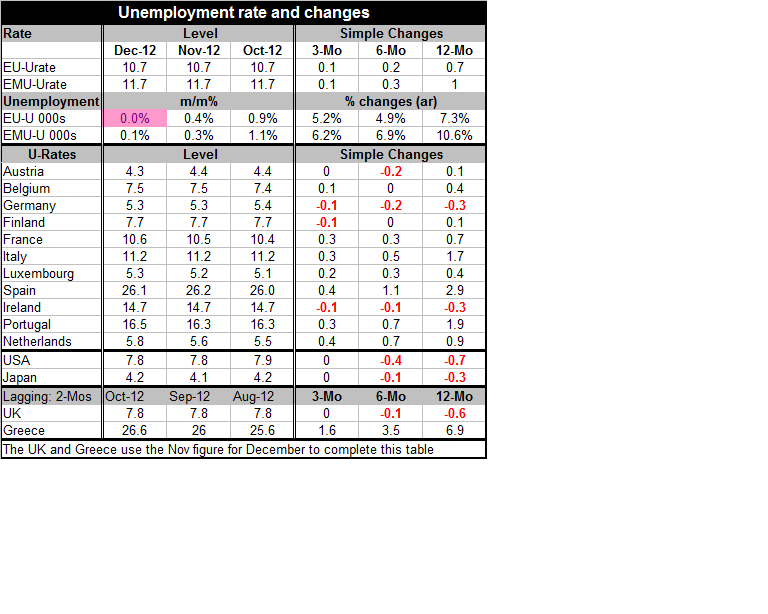

In December the European monetary union's overall unemployment rate and the rate for EMU remained unchanged. For the EU it was at 10.7%; for the European Monetary Union it was at 11.7%. Germany also posted an unchanged unemployment rate between the two months at the comparatively low level of 5.3%

Looking at broader periods, there were declines in the unemployment rate over three months for Germany for Finland and for Ireland, in each case a decline of 0.1% was recoded over three months.

But there were also increases in unemployment rates across countries over three months. The Netherlands and Spain posted increases of 0.4 percentage points in their overall unemployment rate. Portugal, Italy and France saw increases of 0.3 percentage points in their respective rates of unemployment. Luxembourg saw its rate go up by 0.2 percentage points. In Belgium there was an increase 0.1 percentage points. In Austria unemployment conditions were unchanged over three months.

Over short periods of time we get fluctuations and sometimes reversible fluctuations, but changes over 12 months begin to show something that is much more likely to be trend. Over 12 months only Germany and Ireland have net lower rates of unemployment, in each case the unemployment rate fell by 0.3 percentage points over the past year.

Over 12-months, Spain saw an increase in its unemployment rate of 2.9 percentage points. Portugal saw an increase of 1.9 percentage points; Italy experienced an increase of 1.7 percentage points and The Netherlands saw increase of 0.9 percentage points. France had an increase of 0.7 percentage points. Notice that Spain's 2.9 percentage point increase would have more than doubled the German unemployment rate had that happened in Germany.

All of these are fairly substantial increases over the past year; other countries in EMU experienced small increases in unemployment as well, with none of the countries in the table showing 'no change' in unemployment rates over the last 12-month period.

Making a comparison, the United States over the last three months saw its unemployment rate hadn't changed but over the last year the United States sports a 0.7 percentage point decline in its rate of unemployment putting its level on a par with of unemployment in Finland.

Japan also has a decline in of 0.3 percentage points as large a decline as was reported for any of the countries in the table from the European Monetary Union. Japan's unemployment rate is lower than that of any country in EMU.

Still Japan is a very troubled economy, so let's realize that just as Japan is not doing as well as its unemployment rate makes it seem, neither is Germany.

Still, not only is Germany doing better over this time frame than the rest of the European monetary union, but Germany continues to post positive surprises on the unemployment front in 2013. Unemployment in Germany declined unexpectedly in February and for a third consecutive month. This may suggest that the German economy has started to recover in the early months of 2013 after a contraction in GDP in the final quarter of 2012. The number of unemployed in Germany declined month-to-month by 3,000 in February to a level of 2.917 million. This was contrary to expectations for 'no change' in the level of unemployed. In January, unemployment had fallen by a revised 14,000.

The decline in German unemployment helps to explain why German consumer confidence continues to improve. However, the actual rise in German jobs is stunning coming as it does while the rest of Europe is under such pressure from austerity structures that are being tightly enforced by rhetoric from German policymakers. Still it is a stunning fact. It is hard to know how news like this must go down in Italy, in Greece and in Spain, where they are struggling so much and where unemployment already is so high and is moving up further. One thing we can be sure of is that Silvio Berlusconi will know how to handle this information to best help advance his own political ambitions.

The fact of the German performance underscores a long-held position of mine that readers of this research will come to recognize. The biggest problem in the European monetary union continues to be the different levels of competitiveness across members. PERIOD.

While there certainly are other factors like public finances that certainly contributed to the competitiveness differences, competiveness is the problem not the symptom. And fixing it will not be easy.

The lack of mobility in EMU some of it sociologically related because of differences in customs and languages and other behaviors, some of it economic, some of it because of countervailing rules that still tend to limit entry and European competition also can be said to is responsible. But the overriding fact is that since EMU was formed Germany has run a very low rate of inflation and that unit labor costs have hardly risen there while in other countries inflation and unit labor costs have increased tremendously. The further problem is there is no way to put a cap back on this tube of toothpaste and to get the escaped substance back in the tube. It cannot be surprising to see that Italy has candidates running with a platform of looking into re-launch the lira. Why not?

Italy's current account composition and it wealth is such that Italy is one country in the Eurozone the probably could exit with the least amount of pain, a tolerable amount of it. However, were Italy to leave the Eurozone, it would bring an intensification of pressure on other countries to leave, countries whose departure from the Zone would be much more wrenching.

What we are seeing in the Eurozone is something that is typical of what we've been seen in countries around the world. That is that surplus countries cannot be forced change their policies even if it's their policies that are creating the pain.

It took a debt crisis in the European monetary union and in the United States to stop China from its mercantilist export-led growth policy. China country that desperately needed to develop chose to instead to accumulate sterile piles of foreign exchange in order instead of stimulating its own domestic demand. It chose to use domestic demand in the US to drive increases in Chinese output while holding back Chinese consumption and compressing China's ratio of consumption to GDP. Why did China think that was good policy? It worked for China. It gave china and element of control over development and retarded the growth of the middle class keeping dissent at bay. The policy pushed huge deficits onto its selected trade 'partners.' But China was not alone in following that development scheme. Still it was Chain's size and the scope of tis export effort that caused the trade gambit to play out so fast.

Germany plays much the same role within Europe. It continues to limit what could be a better improvement in its living standards in order to keep its inflation rate and its labor costs very low, at competitive levels. Germany thereby sacrifices short-term growth for longer-term stability. Germany is not as large as China and is not trying to raise the size of its economy relative to the world. its objective is quite different from that of China. But like China it seeks persistent trade surpluses. Indeed, Germany is only trying to find equilibrium for a country with a slightly shrinking population growth. Still, the countries of southern Europe seem never to have put off to tomorrow something that could be consumed today. Therein lies the difference for Europe.

It is impossible to think that a region with two such different operating philosophies will be able to bind itself together. From the very beginning the membership made for some strange bedfellows. The difference in the inflation rates that these various member countries had tolerated was well-known before the Zone brought them together in the club. And while some people defend the ECB and its policy as it did (it has) hit its aggregate targets for inflation, the fact of the matter is that neither the ECB nor the European Economic Commission were given any tool by which differences in local inflation rates could be addressed once European monetary Union was formed.

But, in my opinion, that does not mean that neither of those bodies bears responsibility for what happened. Whether your view is that disregarding the Maastricht rules is what was at fault or whether you blame Germany and France for blasting Maastricht out of the water when they violated it (thereby making it irrelevant) the fact of the matter is that entrenched differences in inflation evolved in the zone and nothing was done to change them or even to address them. Europe was blind, deaf and dumb to the phenomenon. Remember this was the biggest publicly discussed sticking point before the union was formed then...silence.

Those differences in inflation have now created deep differences, structural differences within Europe and it's all that Europe can do to stand on its feet and to finance itself from day to day or crisis to crisis. Progress on these issues is not really in train. Europe's answer to Italy's recent electoral obstreperousness is to tell it that 'it' can't afford to backtrack. Europe is trying to make Italy responsible for what happens to Europe should it (Italy) fail but what incentives do the Italians have to make adjustments and bear the burdens for the sake of Europe? What will Europe give Italy in return? Just look at Ireland. Ireland chose to backstop its banks to absorb their bank debt, to put it on the back of the Irish government and to keep Irish bank failures from cascading and pushing losses onto the other banks where they would become the problems for other EMU countries. What has Europe done to help Ireland for having undertaken that burden for the sake of the European monetary union? Basically nothing.

Europe does need to sort out what it can do. It needs to sort out what the EU and the European Monetary Union can do to help give individual countries an incentive to get on a road that will keep the union together. Otherwise it's quite clear that there are member countries whose individual interests are better served outside the union itself. Simply providing help from the European central bank from crisis to crisis and from time to time is not a way to solve the problem in fact it's a way to not solve the problem. Maybe one of these days Europe will come to that same conclusion.

But for now no one in any troubled European nation can see the reason to bear the consequences of such austerity because in part it is unclear what kind of future they buy for themselves if they do that. Do Greeks want to bear extreme pain today so they can live like Germans tomorrow? I bet if that trade off were put to Greece, it would suffer the pain and pull the plug on EMU immediately. Greeks simply are not Germans. Living like a German is not a Greek's ambition. So what do you offer Greece and Italy and Spain...besides nothing at all as an incentive to stay?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates