Global| Mar 31 2017

Global| Mar 31 2017'Lax' ECB Policy Nonetheless Stuffs Toothpaste Back Into the Tube

Summary

Inflation, once galloping headlong toward another case of hyper-Armageddon and toward another I-told-you-so central bank policy screw-up, has suddenly evaporated. Just one month ago German officials were all but howling at the moon to [...]

Inflation, once galloping headlong toward another case of hyper-Armageddon and toward another I-told-you-so central bank policy screw-up, has suddenly evaporated. Just one month ago German officials were all but howling at the moon to convince the ECB to take the pedal off the metal and to at least consider an end to its stimulative ways. Inflation in Germany and in the EMU was on a path to a breach of the 2% mark...at least if you were wearing German-tinted glasses (preferably made by Zeiss, of course), that was how you saw things.

Inflation, once galloping headlong toward another case of hyper-Armageddon and toward another I-told-you-so central bank policy screw-up, has suddenly evaporated. Just one month ago German officials were all but howling at the moon to convince the ECB to take the pedal off the metal and to at least consider an end to its stimulative ways. Inflation in Germany and in the EMU was on a path to a breach of the 2% mark...at least if you were wearing German-tinted glasses (preferably made by Zeiss, of course), that was how you saw things.

Instead the ECB has stuffed the inflation toothpaste back into the tube.

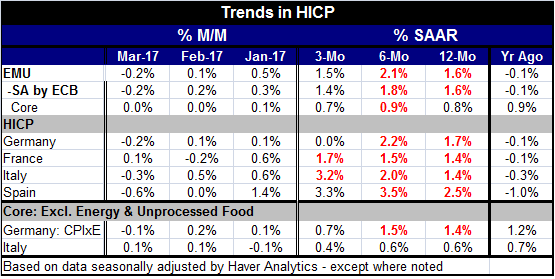

The inflation impulse

German moderate-inflation skeptics (those skeptical that inflation will stay low) have had a lot of company these days as OPECs nascent success in reforming an effective OPEC cartel with the support of 'friends' has paid dividends in pushing up global crude oil prices with all the knock-on effects that implies for petroleum products and all energy-using industries. And those impacts have played out among the various EMU and global price indexes. Measures of 'inflation' have been rising everywhere and in some cases very rapidly, giving fuel to the fire Germans were trying to light under the ECB.

Momentum!

We all know that once inflation gets going, it keeps going. So concerns among inflation hawks everywhere began to mushroom that 'central bankers' had really 'overdone it' this time. And the chickens once again were coming home to roost. And that despite such low inflation as we had experienced to date, we were now on the verge of an overshoot and other such nonsense. Since this, of course, is NOT what is happening, let's look at 'why.'

The No-Tell-Cartel

Instead, of course, the OPEC Cartel once again turned out to be the No-Tell-Cartel. Like the famous motel where no one talks about what went on there (No-Tell-Motel), OPEC members do not discuss frankly what they are actually doing with oil output. Just a few weeks after the Saudi oil minister had lauded his Cartel and Friends for their compliance, he was back giving a fire and brimstone message that members had better adhere to their pump-promises as oil began slipping on global markets. U.S. inventory levels began to look as though there were being contained in their storage units only by the 'miracle' of 'surface tension' as reported inventory levels rose. The rig count in the U.S. was rising and at the same time there were even reports that global growth was doing better. That's a lot of cross currents to keep track of. More oil supply apparently was coming from the U.S., but higher global demand was in gear to soak up more oil as the global PMIs (and other 'soft data reports) turned higher. Still, the clear balance of forces saw oil prices slipping, causing the Saudis to suspect over-pumping and to commission a new Tammy Wynette song "Stand by your pump."

Less than meets the eye

We are all familiar with the expression 'more than meets the eye' to describe events in progress that we cannot see or that have been underestimated. In this case, oil impacting events may been exaggerated. In the U.S., the rig count and actual drilling have expanding faster than oil production has risen. An investigation of this phenomenon shows that rigs on leases may have a requirement that they actually be in use. Oil drillers seem to have been preparing various wells for production, but not actually pumping as much oil as they might have, possibly waiting for even better oil-price levels to evolve before turning on the pump. This tells us that there is a much larger potential overhang from the U.S. from a production increase once prices are deemed 'favorable.' It also takes the U.S. off the hook as the reason for the renewed oil price glut and oil price weakness. That in turn puts the monkey back on the back of OPEC and gives credence to the notion of excess OPEC output. Moreover, the strength in the global economy is not an idea that is bearing as much fruit as thought. This notion of rebound continues to be present more in surveys (or soft data) while hard data from accounting type sources have not filled in with the strength that soft data identified. As an example, U.S. PCE spending in February was a real disappointment, showing an outright decline in real terms. German retail sales fell an outsized 2.1% year-on-year in real terms even as the soft data report 'Eurocoin growth indicator' weakened and Spain's retail sales also came up flat. China's manufacturing PMI continued to add to the good news, but Japan's household spending soured in February even as its unemployment rate fell and production of autos and industrial output overall speeded up. Yes, there are perceptions, exaggerations and, of course, cross currents in the real global economy. But overheating? No.

Yes we have no inflation...

The bottom line is that it appears that beyond OPEC - a Cartel whose sting could yet re-appear- global pressures are still keeping the lid on prices. After a very short-lived push by oil, a push that may have been misread by inflation Hawks and fearful central bankers alike, wary of getting caught with their hands in the cookie jar for too long, inflation is back to a moderate path. In the U.S. the month's PCE deflator and its components' changes for February were tempered despite an adverse base effect that elevated the PCE headline even as the month-to-month inflation pressures were eased.

Europe's fate

The 'Fate of the Furious' is a new auto race movie; it could also be a story about what German inflation hawks will do next, now that their fury which once had no bounds now has no substance. The German HICP is down by 0.2% in March after rising by 0.1% in February and by 0.1% in January. That's not exactly a 'sharknado' of inflation forces. Germany's three-month inflation rate for the HICP is at a compounded annual rate pace of zero. The HICP is still at a 1.7% pace in Germany over 12 months and that compares to only slightly less pressure in the EMU with its gauge up by 1.6% over 12 months. However, the EMU-wide core HICP pace is below 1% over three months, six months, 12 months and over the previous 12 months as well. Italy has reported out a core rate and for Germany we can look at the domestic CPI excluding energy. Both of these 'ex-oil' measures show contained inflation. Germany has made more inflation than in Italy on this basis with year-over-year inflation at 1.4% compared to Italy's at 0.6%. But Germany is the better-growing economy so this is really no surprise. Just today Germany reported a new reunification low for its unemployment rate. Europe will continue to struggle to make policy with countries experiencing such different growth environments. The ECB still has its work cut out for it. And Europe still needs a way to deliver stimulus locally to smooth over differences in regional economic conditions.

Brexit Impact: The Hotel California effect

In the famous Eagles song, "Hotel California," 'you can check out any time you want, but you can never leave.' This appears to be the message from the EU to Britain as the EU seems to want to impose continuing rules on the U.K. even after it has left. But even these only apply after The U.K. swallows a very large and bitter pill of 'euro-reparations' which it is supposed to take without negotiation (no water). It seems clear that this process is going to be very bitter from the outset. The Europeans running the program from the EU side need to look to another Eagles song to have a successful divorce (D-I-V-O-R-C-E, being a Tammy Wynette song) and that is 'Get Over it." Until they do get over it, there will be some real ugliness overhanging the English Channel.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates