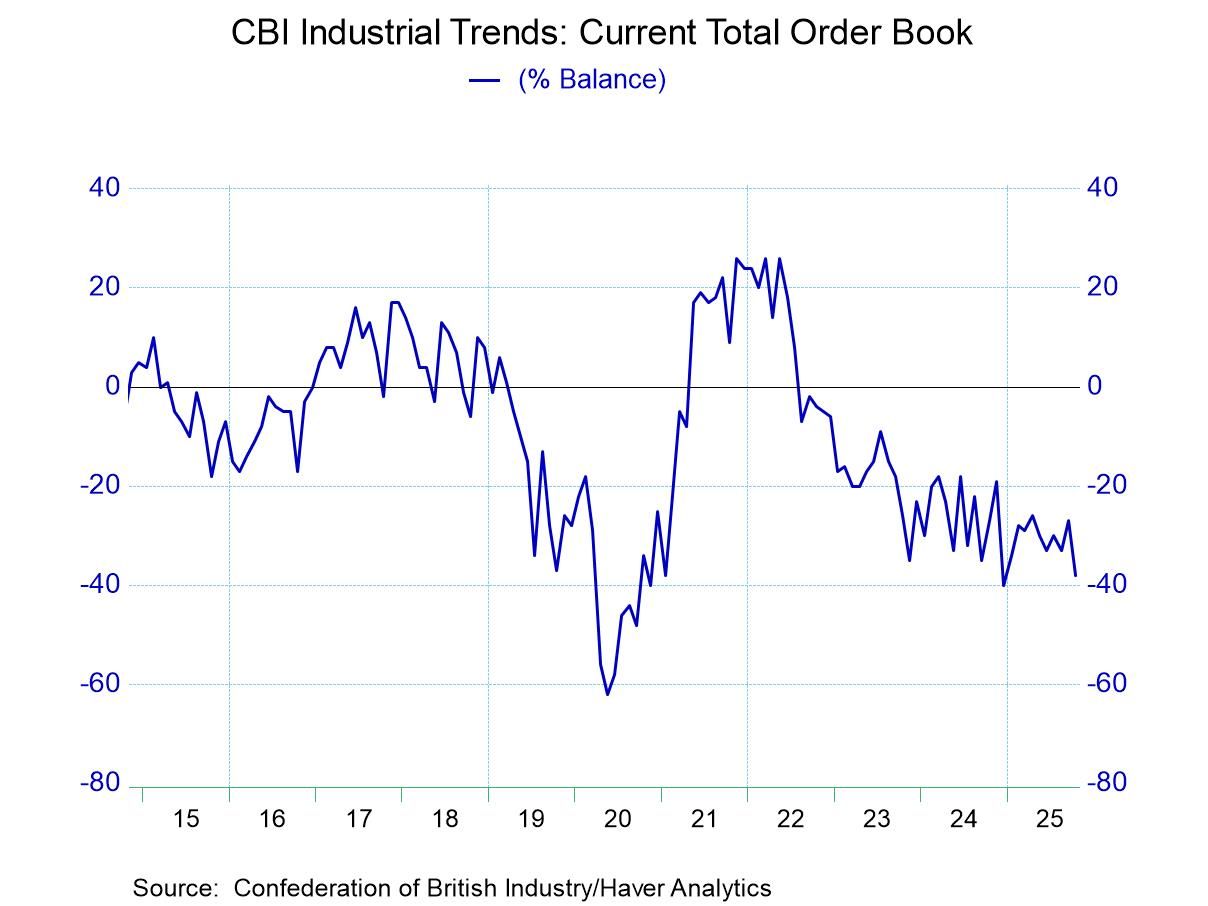

Industrial orders in the United Kingdom fell to a reading of -38 in October from -27 in September this compares also to a level of -33 and August. The 12-months to 6-months to 3-month average progression shows steady deterioration for orders with the 12-month average at a -31 reading, compared to the October reading of -38. Dated back to 1991 the current orders reading ranks in the lower 8% of its historic queue of data, among the observations on that timeline marking this as an exceptionally weak reading on the month and, underpinning the notion, that growth in the UK is weakening and perhaps providing for the Bank of England a way to avoid raising rates in the face of what continues to be excessive inflation.

Export orders also slipped in the month to -46 compared to a reading of -32 in September and -33 in August. Export orders also have deteriorated steadily as the 12-month, the six-month, and the three-month averages are becoming sequentially weaker. Comparisons show the 612-month average at -33 to this month's -46 reading. The percentile standing for export orders is similarly weak to overall orders at a 7-percentile standing.

Looking ahead, the output volume for the next three months finds the index at -19, down from -14 in September and -13 in August. The sequential reading on this metric weakens as well from readings of -9 over 12-months to -12 over 6-months to -15 over 3 months. All that compares to the current October reading of -19. The deterioration there is clearly in place; the queue percentile standing of the October level is at 6%, marking it, once again, as exceptionally weak.

Looking at the prices over the next three months brings an unfortunate increase to 16 from 4 in September and 9 in August. However, the expected inflation results are not on the same deteriorating path as orders trend and expected output. Despite the monthly jump in October, the 12-month average of ‘expected inflation’ is 18, that's reduced to 16 over 6-months and further reduced to 10 over 3 months. The jump in October is a jump that is away from trend, and I suppose we will have to wait to see where it settles in. The trending results for inflation are somewhat more encouraging. The jump in October is quite discouraging although it does come against the background of weakening economic data which simply puts the central bank in a more difficult position to make a policy decision. Price expectations for 3-months ahead have a ranking in their 73rd percentile meaning that they have been stronger a little more than 25% of the time on data back to 1991.

The PMI industrial indicator is up to date through September; here we have a comparison of the manufacturing PMI to the CBI survey. The manufacturing PMI eased to 46.2 from 47 in September. The manufacturing PMI on averages over 12-months, 6-months and 3-months is without a clear trend and has been fluctuating. The manufacturing PMI on data back to 2021 has a 12-percentile standing. The clear message is that conditions in manufacturing in the UK are very weak as the CBI and PMI percentile standings agree. Combined with the CBI inflation outlook, it leaves the BOE in a difficult place.

Global

Global