- FHFA HPI +0.2% m/m (+4.8% y/y) in Jan.; +0.5% m/m (+4.8% y/y) in Dec.

- House prices up m/m in six of nine census divisions but down in South Atlantic and Mountain.

- House prices up y/y in all of the nine regions, w/ the highest rate in Middle Atlantic (8.2%).

USA| Mar 25 2025

USA| Mar 25 2025U.S. FHFA House Price Growth Decelerates in January

USA| Mar 25 2025

USA| Mar 25 2025U.S. Gasoline Prices Strengthen Last Week

- Gasoline costs rise.

- Crude oil prices move higher.

- Natural gas costs stabilize.

by:Tom Moeller

|in:Economy in Brief

Germany| Mar 25 2025

Germany| Mar 25 2025Germany’s IFO Shows Recovery

Germany's all sector climate index improved in March to -19.8 from -24 in February. Still, the index only has a 13.9 percentile standing on data back to the early 1990s. The all-sector climate index, the current index and expectations all improve month-to-month with the scope of improvement for the all-sector climate and expectations indexes greater only about 10% of the time. These are sharp month-to-month improvements. However, the levels of the indexes are so weak that the rankings continue to scrape very low levels. Overall conditions in Germany have hardly changed despite the solid month-to-month improvement concentrated in climate and expectations.

Climate The climate measure shows improvements for the all-sector reading, manufacturing, construction wholesaling, retailing, and services. The highest percentile standing for any sector is for construction at a below-median 41.5 percentile standing. The next highest standing is for retailing at a 24.5 percentile standing, the weakest reading is a standing of 10.3% in manufacturing, and the services sector is at a 13.2 percentile standing, not too much stronger than that.

Transition-Ho! While climate conditions are still in difficult straits, we find that current conditions standings are largely worse than for climate standings; expectations show uneven comparisons. We know there are big changes coming to Europe, particularly for Germany, because of the new shift to more defense spending. This, obviously, will create improvements in the defense sector but should also have broader multiplier effects for the economy, for the manufacturing sector, but also for the economy in general. We also expect these changes to spread across Europe with similar increases in military spending to be introduced in other countries, as the United States is looking for Europe to carry more of its own security burden. We should continue to see improvements in expectations and in climate in the coming months and those improvements should be translated gradually into improved current conditions as well.

Current conditions-Manufacturing and Construction lead Current conditions in the index show improvement across all sectors with minuscule improvements being posted in wholesaling and in retailing in March. The percentile standing for the current indexes in March show the strongest reading in construction; it is the only sector above its median: above its 50th percentile at 61.6%, with retailing close to its 50th percentile mark at 48.2%. The weakest readings are for manufacturing at an 11.9 percentile standing and then services at a 16.9 percentile standing. But manufacturing has the largest month-to-month gain. The overall standing for current conditions is lower still at its 10.7 percentile standing, indicating a confluence of weakness across sectors, a result that has the overall index at a weaker standing than any for individual sector.

Expectations – Manufacturing surges Expectations show broad improvement and for the most part fairly significant improvement across sectors. The headline improvement shows expectations at -16.1 in March compared to -20.5 in February, which leaves the index at a 16.9 percentile standing overall. Expectation standings are weak, however, with the strongest expectation standing in manufacturing at 21.1%, the second strongest for wholesaling at 19.8%; services rank third with the standing of 15.1%. Construction, the sector that has the strongest current and climate standings, has the weakest expectation-standing at the 8.2 percentile mark.

USA| Mar 24 2025

USA| Mar 24 2025Chicago Fed National Activity Index Rebounds in February

- Index recovers January’s decline.

- Three-month average surges.

- Half of components rise.

by:Tom Moeller

|in:Economy in Brief

Global| Mar 24 2025

Global| Mar 24 2025S&P Flash PMIs-Services Worse, Manufacturing Better

S&P flash PMI statistics for March show very little change in the composite which has been plugging along at 51.4 in January, 51.4 in February and now 51.5 in March. These are readings from unweighted averages from the eight reporting countries and the European Monetary Union. The manufacturing composite is crawling its way higher from 49.1 in January to 49.5 in February to 49.9 in March, putting manufacturing nearly to a breakeven reading after a long period of showing sector contraction. Service sector readings monthly log 52.0 in January, 51.9 in February and 51.6 in March, a steady but very minor trend to erosion.

The sequential growth rates on the quarterly average readings that exclude March are performed only on hard data. They show that the composite reading has also been very stable at 51.6 for the 12-month average, 51.3 over 6 months and 51.3 over the most recent hard 3 months’ worth of data. Manufacturing has also been stagnant with a reading of 48.4 for the 12-month average, 48.4 for the six-month average and 48.6 for the three-month average for the period ended in February. Services show the same minor slippage we see in the monthly data from 52.5 over 12 months to 52.2 over 6 months, to 52.0 over the most recent three-months of hard data. These trends show minor improvement in manufacturing and minor deterioration in services. Manufacturing continues to show minor contraction as services continue to show minor expansion. Neither sector performs particularly well and neither sector has any particularly notable trend to it. The diffusion data across countries show a great deal of variation.

Asia| Mar 24 2025

Asia| Mar 24 2025Economic Letter from Asia: Reciprocity

This week, we explore the growing impact of recent US policy moves—particularly President Trump’s “reciprocal” tariffs scheduled for April 2—with a spotlight on their implications for Asia. The effects of China’s retaliation to the US’s first round of 10% tariffs are already visible in the data (Chart 1). Similarly, in South Korea, the Biden administration’s tightening of chip export restrictions has likely contributed to a slump in the economy’s recent semiconductor exports to China (Chart 2). Despite these challenges, investor concerns about Trump’s upcoming "reciprocal" tariffs have been eased by reports suggesting they may not be a blanket measure, with certain economies potentially exempt. While the potential impact of these tariffs on Asia may initially seem significant, the effects are likely to be concentrated in a few economies, particularly India. This is mainly because, India still maintains one of the highest average tariff rates in the world (charts 3 and 4), despite progress in reducing tariffs over the years (Chart 5). In contrast, South Korea, though it has a relatively high average tariff rate, benefits from a very low effective tariff rate on US imports (Chart 6), thanks to its bilateral trade agreement with the US.

Tariff effects on China Earlier, China responded to the US’s first round of 10% tariffs on Chinese imports by placing tariffs on certain energy products and large-engine cars from the US. The effects of these tariffs are already evident in the data, as shown in chart 1. Specifically, China’s imports of US cars have continued to decline sharply, and its imports of certain energy-related products have also decreased through the year so far. However, China’s overall imports from the US have increased on a year-over-year basis. Looking ahead, investors are likely focused on the impact of China’s second round of retaliatory tariffs, which mainly target US agricultural goods.

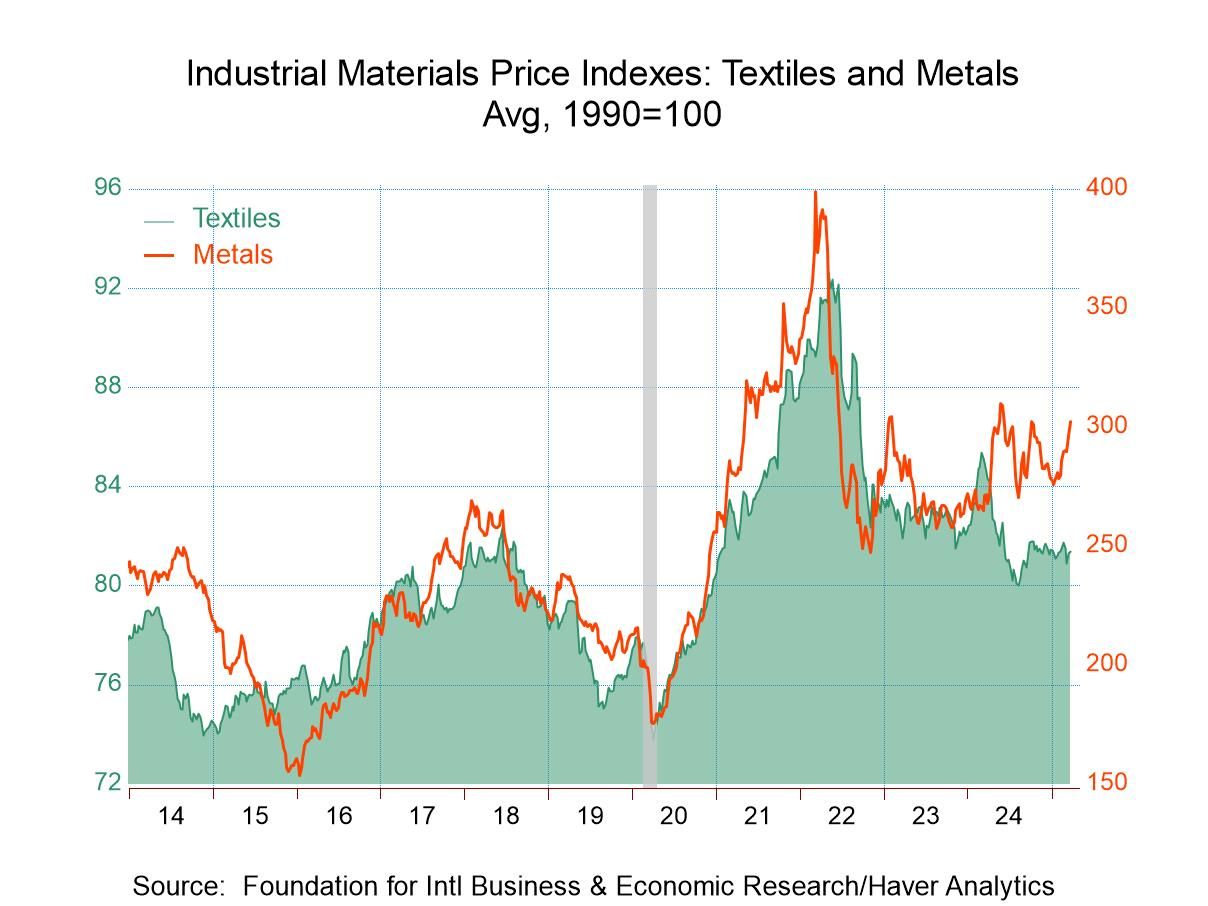

- Metals prices surge.

- Lumber prices strengthen.

- Crude oil costs decline.

by:Tom Moeller

|in:Economy in Brief

France| Mar 21 2025

France| Mar 21 2025INSEE Manufacturing and Services Steady-to-Weaker

The INSEE industry climate index settled lower in March at 95.9, down from 97.0 in February. The index is lower than its year-ago value of 102.1 and since 2001 it has been this low or lower only 7.5% of the time. Despite the sense of some stability in manufacturing in the tabular data for the last year, the chart (of data since 2014) and the table’s own presentation of the queue standing reveals manufacturing to be at a relative weak standing in March.

Manufacturing production expectations have a 34.4 percentile standing but did improve slightly from the February reading of -14.8. The recent trend of production weakens on the month to a lower quartile standing at its 23.7 percentile. The personal likely trend, which is the reading for each respondent gives to the prospects for his own industry, ticked higher in March to a 40.5 percentile standing. That is better than the percentile for industry over all but still below the level that marks the historic median – a standing at the 50th percentile.

Orders and demand as well as foreign orders and demand each weakened. They each have standing at or below their respective 20th percentile around the lower one-fifth of all historic readings. In addition, the March reading for orders and demand are substantially weaker than they were a year ago and the slippage has been worse for foreign orders.

In contrast, inventory level show few changes and are similar to their year-ago readings and close to their historic median.

Prices have moved to lower readings in recent months. However, price trends and level readings are higher than they were a year ago. In terms of rankings, the own likely price trend is at a 61.5 percentile standing, above its historic median while the manufacturing price level has a relatively weak 36.1 percentile standing.

- of2693Go to 87 page