Financial market volatility has remained elevated over the past several days as investors attempted to weigh a modest improvement in sentiment—driven by a potential, if partial, retreat by the US administration from its aggressive tariff stance—against a still-cloudy global outlook. Signals from flash PMI surveys on global growth remain mixed: Europe continues to stagnate, with the UK particularly weak, while India stands out with resilient and rising manufacturing activity (chart 1). In the US, most of the incoming data suggest that business confidence has faltered, with capital expenditure intentions plunging particularly sharply in the wake of the April 2nd tariff announcement (chart 2). The drag from trade tensions is, moreover, becoming more evident: South Korea’s exports have slumped, especially to the US, and even sectors granted exemptions—like semiconductors—are showing signs of strain (chart 3). These pressures are reverberating through financial markets as well, where Chinese investors are shifting into gold as a hedge, fuelling record trading volumes on the Shanghai Gold Exchange and lifting global gold prices (chart 4). Meanwhile, a broadly-based decline in the US dollar and persistently high readings on the VIX index arguably reflect a deeper reassessment of US assets as reliable safe havens amid mounting policy unpredictability (chart 5). Beneath these short-term ripples lie more entrenched structural challenges: the US is seeking to rebalance away from external deficits linked to its reserve currency role, while China is under growing pressure to pivot toward consumption-led growth—an imperative sharpened by American efforts to choke off its export strength (chart 6). In short, the latest softening in US trade rhetoric may offer brief relief, but the underlying economic, geopolitical, and structural crosswinds remain very much in play.

Global| Apr 25 2025

Global| Apr 25 2025Charts of the Week: Dollar Dips and Trade Trips

by:Andrew Cates

|in:Economy in Brief

More Commentaries

USA| Apr 24 2025

USA| Apr 24 2025U.S. Unemployment Insurance Claims Hold Fairly Steady

- Initial claims equal the 222,000 forecast amount

- Continuing claims ease modestly; prior week revised down somewhat

- Insured unemployment rate maintains longstanding 1.2%

France| Apr 24 2025

France| Apr 24 2025French Household Sentiment Marks Time

Household confidence in France has steadied after along climb up from an historically weak level. Still, confidence has only a 36.5 percentile standing.

Living standards show mixed changes this month. Standards compared to the past 12 months are a bit better month-to-month, while looking ahead, they are weaker and fall by 3 survey points.

However, unemployment expectations have moved sharply higher for the month, rising to 51 in April from 47 in March, to a very high percentile standing at the 70.4 percentile mark.

Price developments are moderating with weaker readings compared to 12 months ago. The percentile standings for prices, however, are modest, below the 50-percentile mark, showing these are below median readings both looking backward and looking ahead.

The savings environment has worsened both on backward-looking and forward-looking savings responses. And the rankings for these environments are both very high.

The saving environments dove-tails with a spending environment that did improve on the month, remains weak, and has a ranking at its 34th percentile. The environment is very favorable to save and not very favorable to spend.

The financial situation is little-changed in the month either looking-forward or looking-backward. That is a rather odd result, given the uncertainty over tariffs; but then maybe when policy causes uncertainty viewpoints freeze. On a month-to-month comparison, we see stronger financial situation ranking looking back 12-months that has an above median percentile standing at 65.4; but looking ahead there is a below median standing at the 44.2 percentile.

The table also presents two columns tracking the economic shock from before Covid to before the Russian invasion of Ukraine and secondly from that point to date. What this shows generally is that at the time of the invasion, most of the survey items had improved upon their pre-Covid readings. One exception is that unemployment concerns were still further elevated. But then from pre-invasion forward, most readings are substantially weaker. But in comparison, the change in unemployment is strikingly higher.

On balance, France’s household responses seem to exhibit some stickiness that may be a product of uncertainly. The overall readings remain weak.

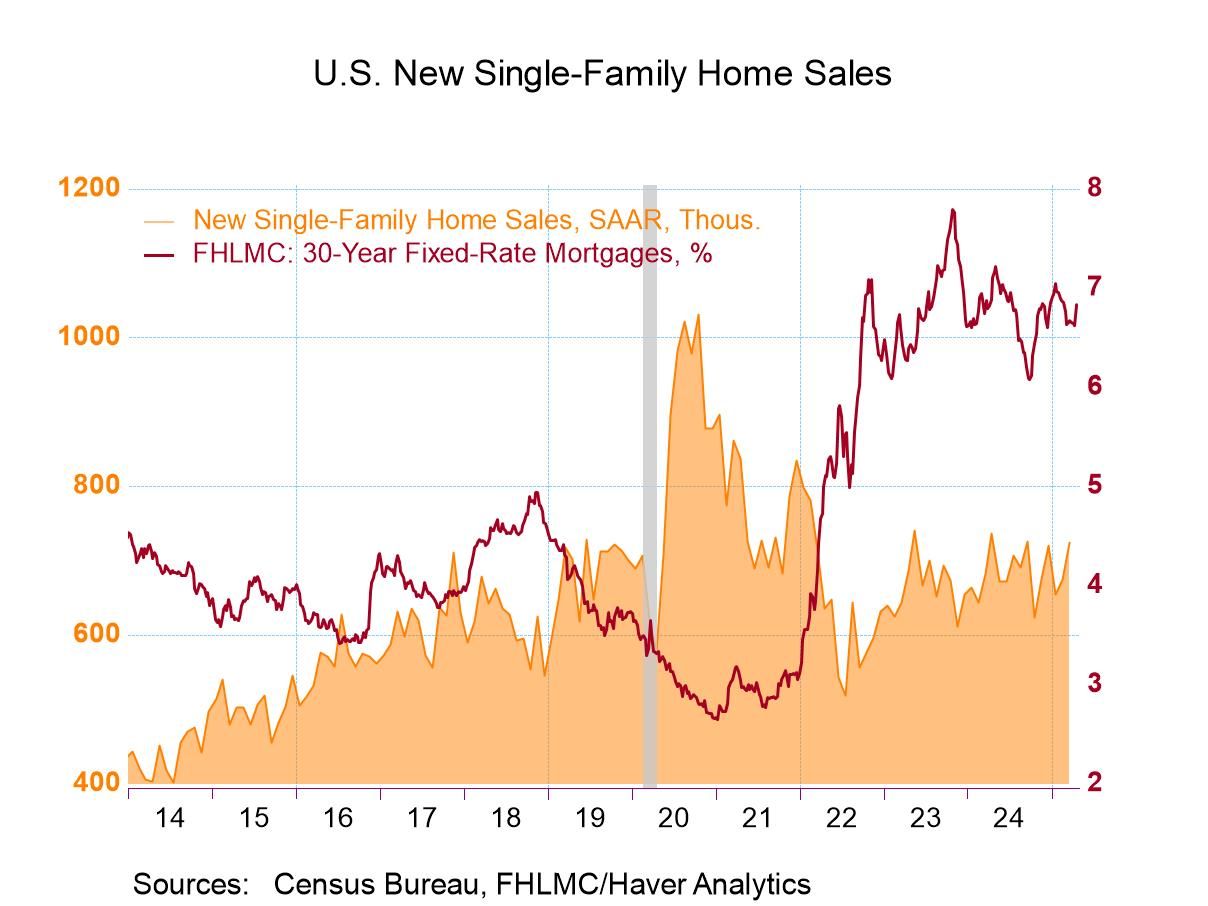

USA| Apr 23 2025

USA| Apr 23 2025U.S. New Home Sales Improve in March; Prices Weaken

- Sales rise to highest level in six months.

- Changes in sales are mixed across the country.

- Median sales price falls to four-month low.

by:Tom Moeller

|in:Economy in Brief

- Refinancing loans fall sharply and purchase loan applications decline as well.

- Effective interest rate increases to two-month high.

- Average loan size falls sharply.

by:Tom Moeller

|in:Economy in Brief

USA| Apr 22 2025

USA| Apr 22 2025U.S. Energy Prices Are Mixed in Latest Week

- Gasoline prices fall sharply again.

- Crude oil prices edge higher.

- Natural gas costs decline further.

by:Tom Moeller

|in:Economy in Brief

Denmark| Apr 22 2025

Denmark| Apr 22 2025Danish Confidence Drops to 2-Year Low; Inflation Concerns Remain Elevated

Danish confidence slipped to -17 in April from -15.5 in March, continuing a slide that extends back to late-2023. The weakness accelerated in late-2024 especially with the conclusion of the U.S. elections.

On data back to late 1995, the consumer confidence indicator for Denmark ranks in its lower 3.7 percentile. Confidence has been higher than this most of the time over this period.

The financial situation over the past 12 months ranked at a weak 7.3 percentile standing, but for the next 12 months an even weaker 1.4 percentile reading is in place. The existence of U.S. tariffs and pushback for Europe to carry more of its own defense burden seem to be adversely impacting Danish sentiment. There may also be some anxiety stemming from President Trump’s stated desire to have Greenland, a semi-autonomous Danish territory, become part of the United States.

The general economy has a confidence ranking at its 13.8 percentile over the last 12 months, but that drops to an all-time low ranking of zero for the next 12 months. All these respondents backed down in April compared to their March readings. The ‘expected’ financial conditions response fell by the most.

In sharp contrast, consumer prices for the last 12 months carried a 92.7 percentile standing; for the next 12 months, that pushes back up to the 98.6 percentile. Meanwhile, unemployment concerns, while ticking lower, have a standing at their 84.6 percentile higher since 1995 less than 16% of the time.

The environmental readings show the favorability of the time to purchase or save for the next or last 12 months (four metrics) all generate readings below their respective median (below a standing of 50%. The time to purchase readings are the weakest in this group.

However, the general financial situation for households currently holds above its historic standing at a reading with a 54.5 percentile standing. But that reading eroded last month.

- Metals prices weaken broadly.

- Lumber & rubber prices fall.

- Crude oil prices remain soft.

by:Tom Moeller

|in:Economy in Brief

Global| Apr 17 2025

Global| Apr 17 2025Charts of the Week: From Blue to Red

U.S. policy decisions have sparked a sharp rise in financial market volatility in recent weeks, reflecting mounting investor unease about the global economic outlook. Consensus forecasts for growth in 2025 have been revised down significantly, while inflation expectations—particularly in the US—have moved higher, highlighting the stagflationary risks associated with the sweeping tariff measures introduced in early April (Charts 1 and 2). Although these actions have since been partially rolled back, the broader shift toward protectionism is already disrupting global trade flows and could soon feed through to consumer prices, compounding the challenge for central banks already struggling with sticky inflation. In parallel, measures of financial market stress have climbed to multi-month highs as investors reassess risks in an increasingly fragmented and uncertain environment (Chart 3). Business sentiment has also deteriorated notably, with this week’s Empire State Manufacturing Survey showing a collapse in forward-looking expectations (Chart 4). Adding to concerns, global shipping costs have begun to rise again, raising the risk that renewed supply chain frictions will put upward pressure on goods inflation across advanced economies (Chart 5). Finally, in China, hopes for stabilization in the property sector are fading. Despite some recent stabilisation in house prices, real estate investment continues to contract sharply, suggesting that structural headwinds remain firmly in place (Chart 6). Taken together, this week’s charts point to a fragile global economy contending with greater protectionism, rising inflation risks, weakening business confidence, and subdued demand—all of which are reinforcing the ongoing malaise in investment sentiment.

by:Andrew Cates

|in:Economy in Brief

- of2616Go to 1 page