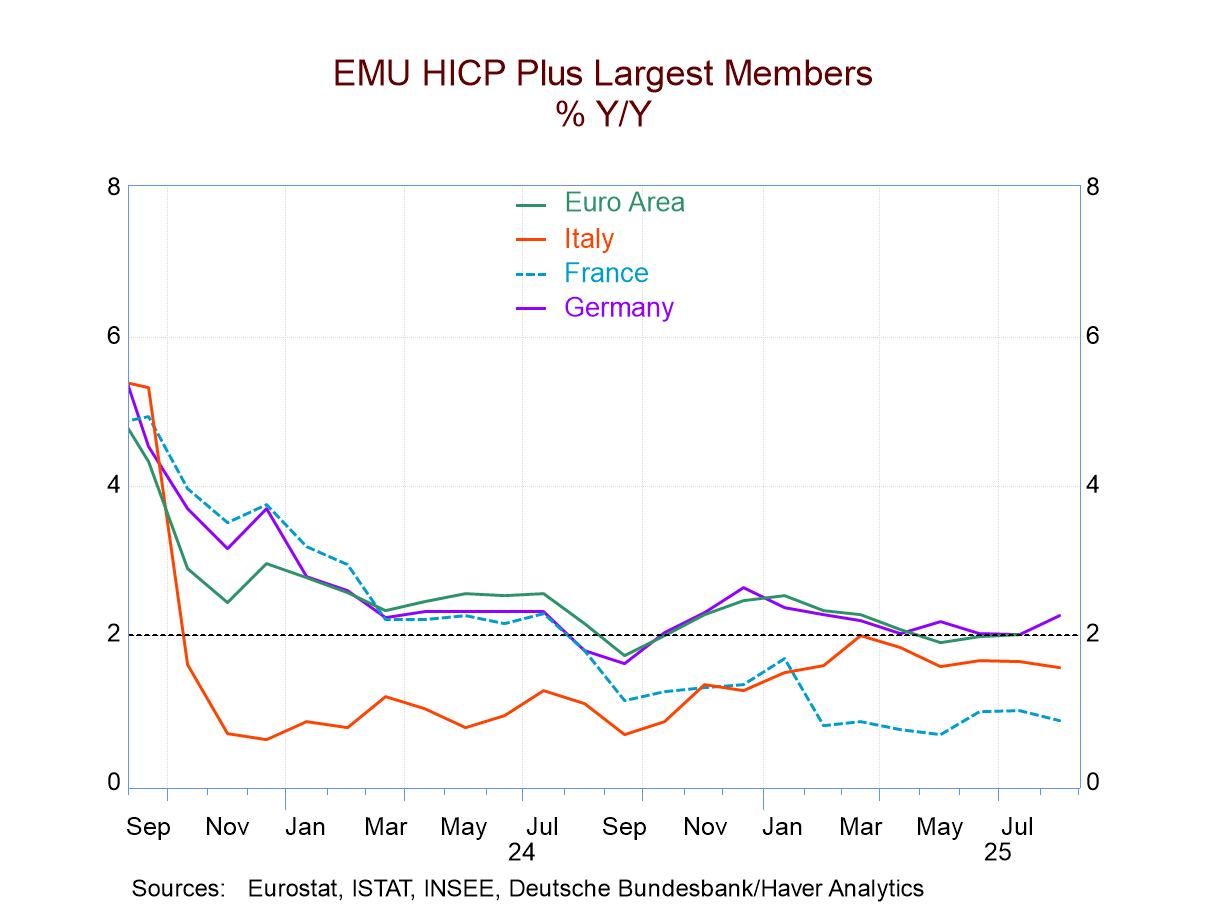

Inflation in the monetary union was tepid across the large, early-reporting, economies in August. The HICP rose by 0.2% on the month in Germany, rose by 0.1% in France, while it was flat in both Italy and Spain. However, these outstanding readings followed several months of stronger inflation; in particular in July German prices rose by 0.2%, in Italy the gauge rose by 0.3%, in France by 0.4%, and in Spain by 0.5%.

As a result, over three months, inflation is running hot on the headline gauge, over 2% in France, Italy, and Spain, and just below it, at a 1.8% annual rate in Germany. Over 12 months, inflation is well behaved, but that headline is up 0.8% in France, rises by 1.7% over 12 months in Italy, by 2.1% in Germany, and at a 2.6% pace in Spain. That is a bit more mixed but still quite solid set of results. The EMU-wide HICP for July – on a one-month lag- rises by 2.1% over 12 months with a core at 2.3%.

Core inflation is not well reported on an early basis. The Italian core rate rose 0.2% in August with Spain at 0.3%; both Italy and Spain logged increases of 0.3% in July and in June and as a result the 3-month inflation rate on the core for Italy and Spain runs at 2.7% in Italy and at 3.8% for Spain. These, of course, are much higher and more disturbing numbers for inflation. The 6-month inflation rate for core Italy and Spain runs at 2.9% and 3.1%, respectively, while over 12 months the Italian core is up by only 2.1% and the Spanish core is up by only 2.4%. The kick up and inflation for the core is a relatively recent phenomenon.

Global

Global