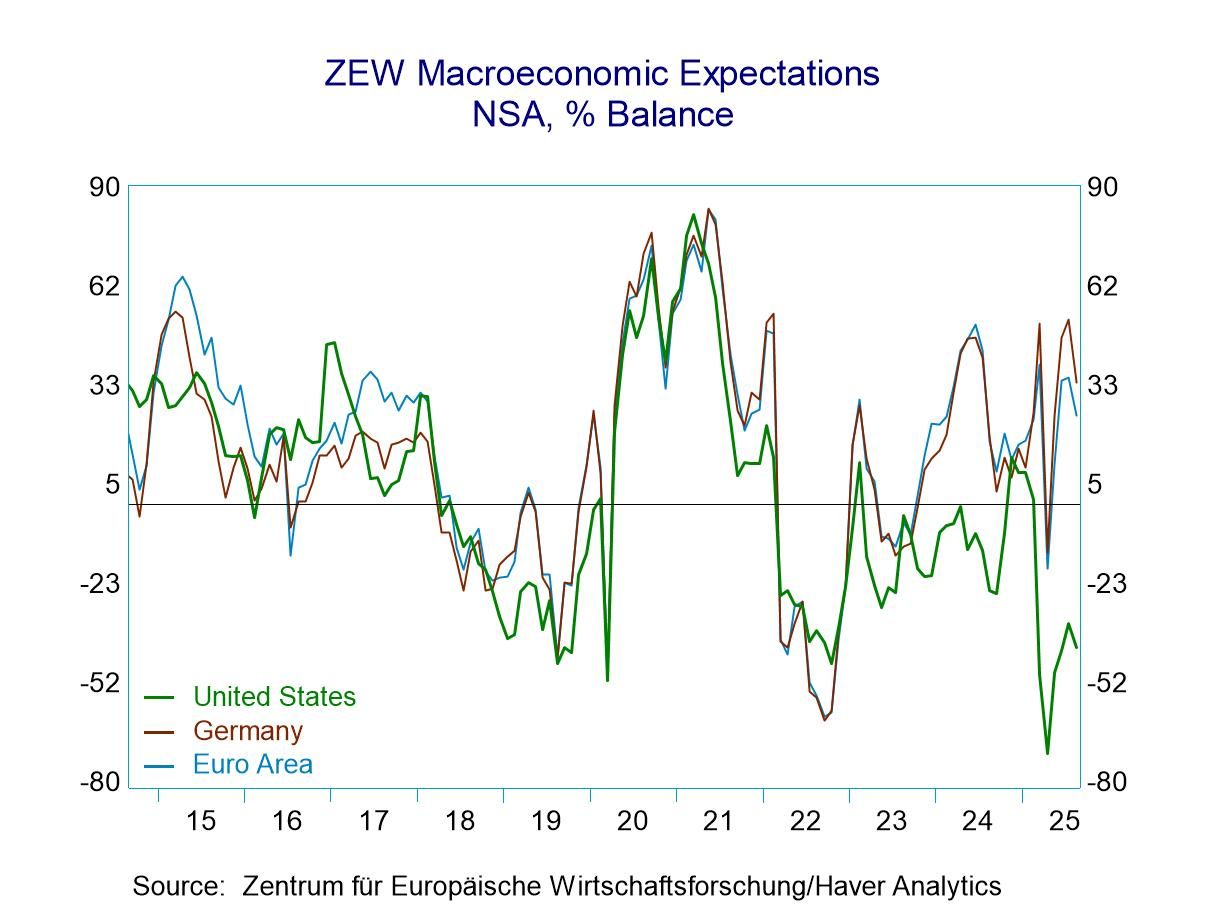

Global

GlobalMacro-expectations- The ZEW financial experts registered disappointment this month in the tariff deal that the European Community struck with the United States. Macroeconomic expectations in August for Germany were slashed back to a reading of 34.7 in August from 52.7 in July; for the United States, expectations also were cut to -41.2 from -34.2. These two sets of reductions brought German expectations to a 60.8 percentile standing, leaving them still above their median on data back to the early 1990s. The U.S. reading has a much lower, 9.3 percentile standing on the same timeline. Despite the ZEW experts’ opinion that the tariff deal is bad for Europe, it apparently doesn't boost expectations for the U.S. at all. This, of course, makes me wonder to what extent the forecast has a bit of sour grapes to it.

The economic situation- The economic situation also deteriorates this month with the euro area assessment falling to -31.2 from -24.2 in July. Germany's assessment falls to -68.6 from -59.5 as the tariff deal weighs on Europe and Germany. The current situation for the U.S. improves marginally to +0.1 in August from -5.9 in July. These new readings leave the euro area economic situation reading with a ranking in its 46.9 percentile, Germany ranks in its 22.2 percentile, and the U.S. stands in its 35.1 percentile.

Inflation expectations- Inflation expectations in Europe remain low but increased to some extent in the U.S. where they were already high. The European readings for the euro area fell back to -6.7 in August from -5.8 in July. For Germany, the reading was little changed at -5.1 in August from -5.2 in July. The U,S, rating moved up to +74.5 in August from +64.3 in July. The queue standings for these metrics show the euro area inflation expectations standing in its 27th percentile, the same as for Germany, but for the United States inflation expectations are up to their 95.9 percentile! This is an extremely interesting angle from the ZEW financial experts because we have the Fed in the U.S. poised to cut interest rates. We have the President pushing the Fed to cut interest rates more quickly and more deeply than it wants to do it. And despite the fact that inflation has run over target for four and a quarter years in the U.S., we have the Fed seemingly ready to cut interest rates, perhaps twice by the end of the year, even with the potential for inflation from tariffs knocking at the door. The ZEW experts ‘take’ on the U.S. and its financial situation seems to be quite different from how it's being analyzed in the United States.

Short-term interest rates- Short-term interest rate expectations for the euro area show less of an inclination for rates to fall with the -35.7 reading in August compared to -49.7 in July. For the U.S., the -61.5 reading is lower than July's -43.8, indicating that expectations for rate cuts in the U.S. are growing. The euro area short-term rate expectation has an 18.4 percentile standing whereas in the U.S. the standing is at its 10.4 percentile.

Long-term rate expectations- Long-term interest rates found reductions both in Germany and the U.S. in August. German expectations fell to an index reading of 19.0 from 26.1 in July. In the U.S., the reading fell to 26.4 from 38.7. The queue standings for the German rate are in their 25.5 percentile, below the U.S. where the percentile standing is at its 32nd percentile. In both cases, the expectations for long rates indicate a good deal of moderation. Queue standings well below their respective median readings for both Germany and the U.S. (remembering that the medians for ranked data occur at the 50th percentile mark).

Stocks- Stock market expectations were slightly weaker in Europe with the euro area falling to 18.1 in August from 22.4 in July. The German reading fell back to 18.5 from 24.6, while the U.S. reading is little changed at 8.4 compared to 8.6 in July. The standings for all of these readings are around the 15th percentile; there are small differences among the different reporters, but nothing of significance.