- CFNAI -0.12 in August, highest since March; -0.28 in July.

- Three of four CFNAI components up m/m, but three make negative contributions.

- CFNAI-MA3 improves to -0.18, the fourth straight negative reading; still above -0.70 (recession signal).

- CFNAI Diffusion Index increases to -0.24, highest since April.

Belgium| Sep 22 2025

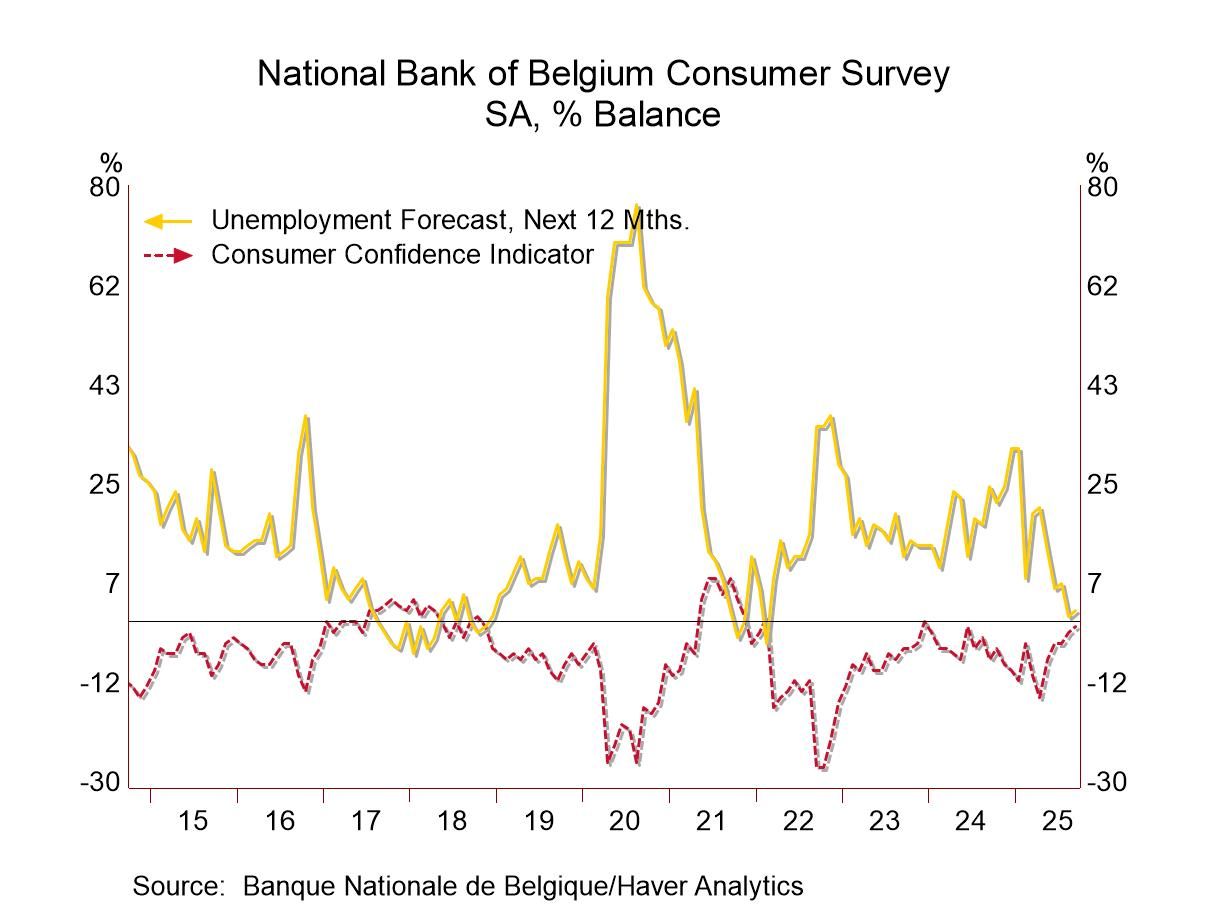

Belgium| Sep 22 2025Belgian Consumer Confidence Makes Modest Gain; On a Slow Improvement Track

This steady progression is underpinned by a six-month-ago reading of -10 and a 12-month-ago reading of -7. Belgium is an interesting mid-European economy. It is industrialized, it is middle-sized and it's in the middle of the monetary union itself.

When the performance of confidence in Belgium is compared with the European Monetary Union total, we find that there is an average correlation in confidence of 0.56 across seven key economies including the monetary union measure itself. Belgium has a 0.79 correlation with confidence in the Netherlands, 0.69 relationship with France and the 0.76 correlation with the EMU overall, so it's a reasonably consistent bellwether for what's going on in the monetary union. And the correlation is close to 0.5 with Italy and Portugal. Belgium's weakest correlation in the monetary union among these countries is 0.18 with Greece. This suggests to me is that Belgium is a country that's relatively plugged into the activity trend of the monetary union itself.

Belgium’s ranking for consumer confidence at 78.8% on data back to 1991; since January 2020, its consumer index is up by just 5 points, a very shallow gain for such a long period of time – but still a solid and firm ranking.

For the economic situation over the next 12 months, the reading has a ranking at its 17th percentile, substantial steep down from a 40th percentile standing of the past 12 months. That’s not a good sign.

Price trends are slightly elevated on a ranked basis but are falling month-to-month from July to August to September. However, sequentially since 12 months ago, they are on the rise- so the inflation picture is more complicated. Expected inflation (price trend) at a 69th percentile standing for the next 12 months, is down from what is now a 77.9 percentile standing over the previous 12 months.

However, unemployment expectations are mild and falling both short term and sequentially with a low 9 percentile queue standing. That is very good news.

The financial situation of households is little changed on both short- and long-term trends with modest near median ranking for the next- was well as the last-12-months.

The appraisal of the current situation is down a notch in the month and sequentially has eased a bit as well but stands with an 83.2 percentile ranking, one of the highest standings in the table.

Household standings have a high 94.4 percentile standing, the favorability to save at the 74.6 percentile mark.

On balance The Belgian readings are solid and mostly upbeat. Inflation readings show concerns more than fear about what might be happening on the price front. On the whole, the response standings and trends are a positive signal for this country set in the belly of the European Union.

Asia| Sep 22 2025

Asia| Sep 22 2025Economic Letter from Asia: Of Politics and Policy

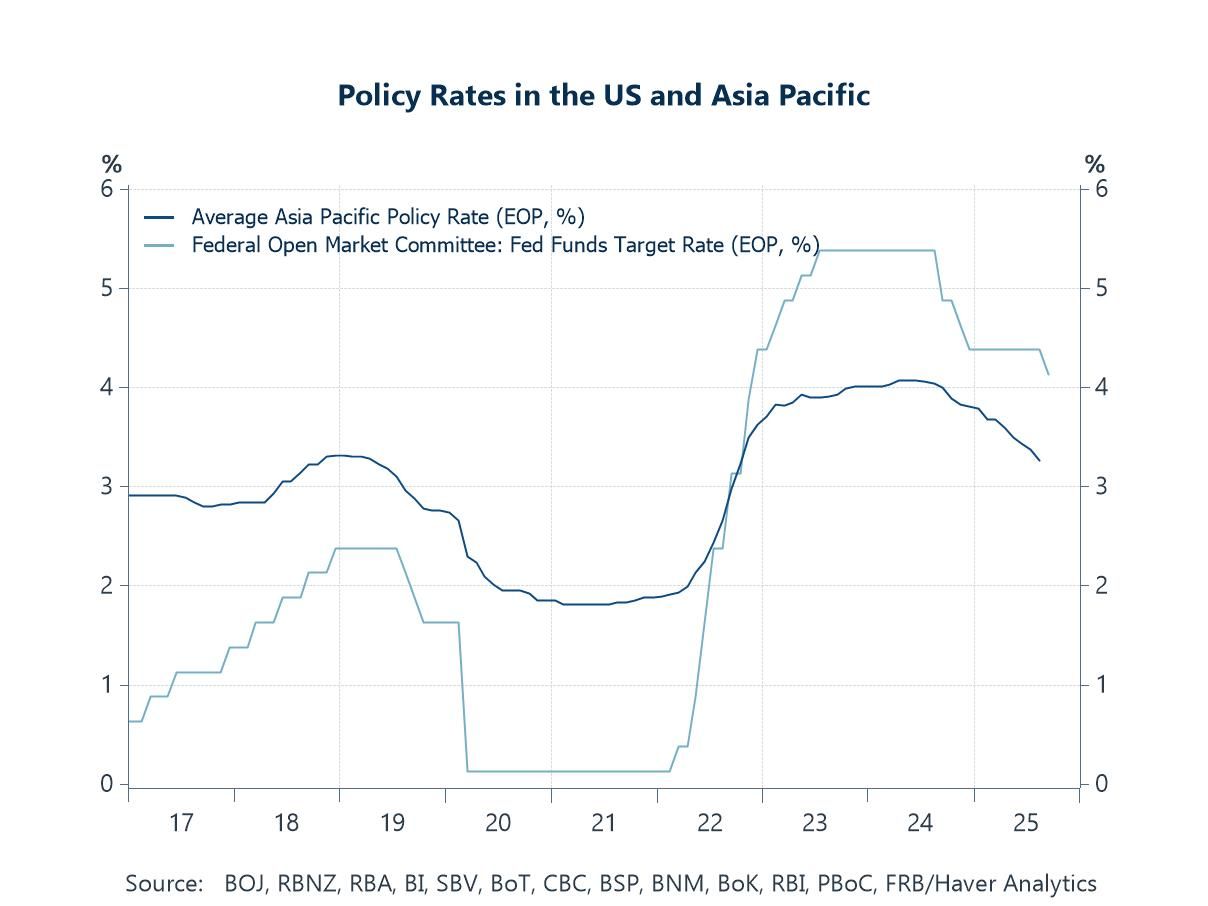

Following last week’s decision by the Fed to lower US interest rates, we examine Asia’s economic outlook, with particular focus on Japan, Indonesia, and Thailand. The Fed’s first rate cut of the year—while signalling more to come—has cleared the path for further easing from Asia’s central banks. Still, many regional central banks had already loosened policy despite wider yield differentials, responding to sluggish domestic demand, the growth drag from new US tariffs, and muted inflation pressures (chart 1). Across Asia, moreover, political turbulence risks distracting governments from tackling deeper structural challenges.

In Japan, the BoJ kept its policy rate unchanged as expected last week but announced the gradual unwinding of its large ETF and J-REIT holdings, a move likely to tighten liquidity (chart 2). On the political front, investors are watching the LDP’s two-week leadership contest, which culminates in an October 4th vote, with elevated food costs and broader inflation still pressing concerns (chart 3). Indonesia remains in focus as well, with investor concerns over fiscal discipline heightened by the recent removal of its long-serving Finance Minister. Long-standing issues, such as persistently high youth unemployment, continue to weigh as well (chart 4).

Thailand faces its own political uncertainty, with elections expected within four months after Prime Minister Anutin’s appointment. The interim push for near-term policy wins risks delaying structural reforms on household and public debt (chart 5). Meanwhile, the baht’s recent sharp appreciation—driven partly by surging gold prices (chart 6)—is straining exports and tourism, prompting the Bank of Thailand to explore measures to ease the currency’s gains, including taxing gold and encouraging US dollar-denominated trades.

Post-Fed reactions, implications As expected, the Fed cut its policy rate by 25 bps at its September meeting, marking its first reduction of the year after months of anticipation. The updated “dot plot” suggests two additional cuts may be on the horizon, though these projections remain data-dependent. The Fed’s move follows several rounds of easing by Asian central banks (chart 1), which cut rates despite wider US differentials to shore up weak domestic demand or offset risks from US tariffs. Contained headline CPI, driven by softer demand and the absence of broad supply shocks, has given the Asian policymakers room to ease. Looking ahead, further rate cuts across Asia—except in economies such as Japan, which maintain a tightening bias—remain possible. This is especially likely as the growth effects of the latest US tariff hikes, effective August 7th, have yet to be fully felt. If the Fed delivers additional easing later this year, it could further strengthen the case for Asian central banks to loosen policy again.

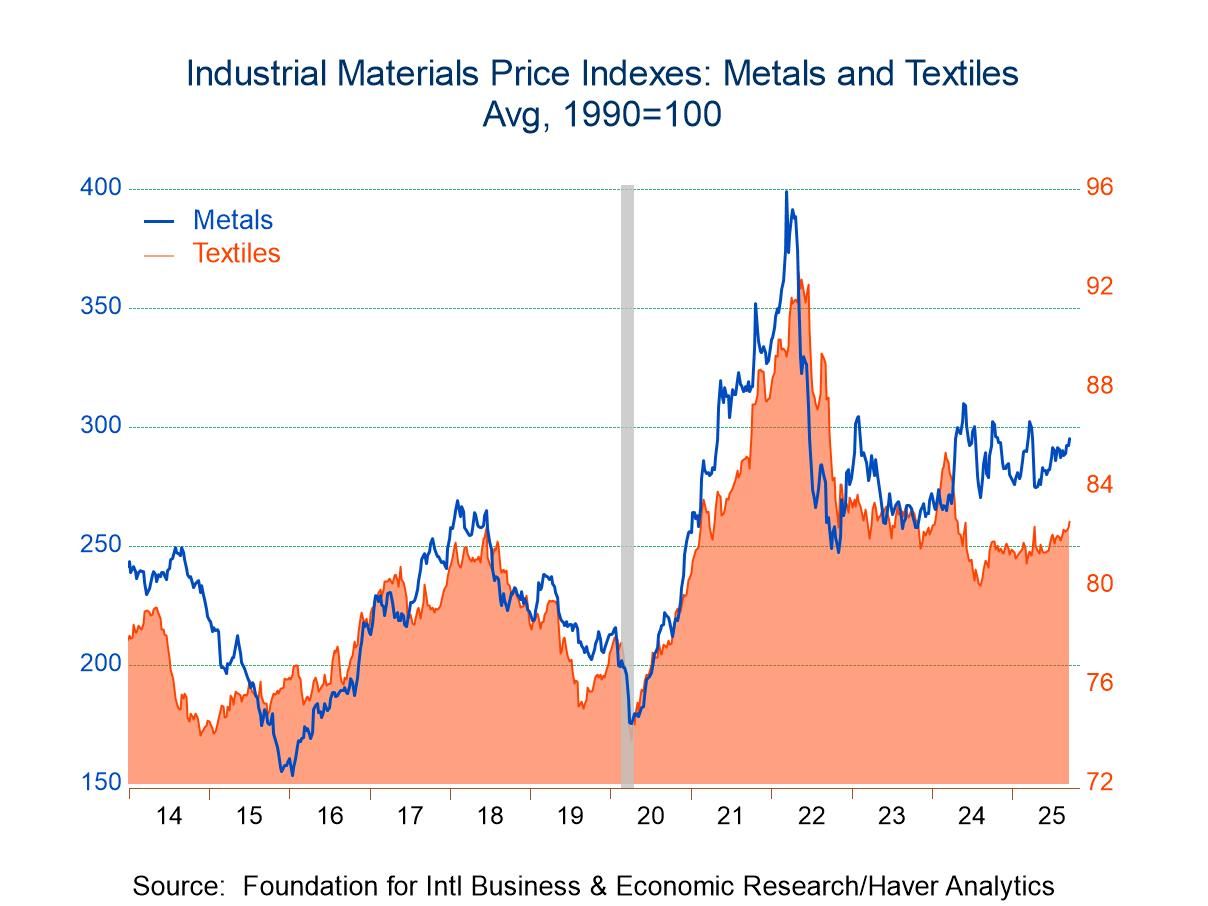

- Slight rise is first since early August.

- Metals prices strengthen while textile costs improve.

- Lumber & crude oil prices decline.

by:Tom Moeller

|in:Economy in Brief

Germany| Sep 19 2025

Germany| Sep 19 2025German PPI Shows Ongoing Release of Inflation Pressure

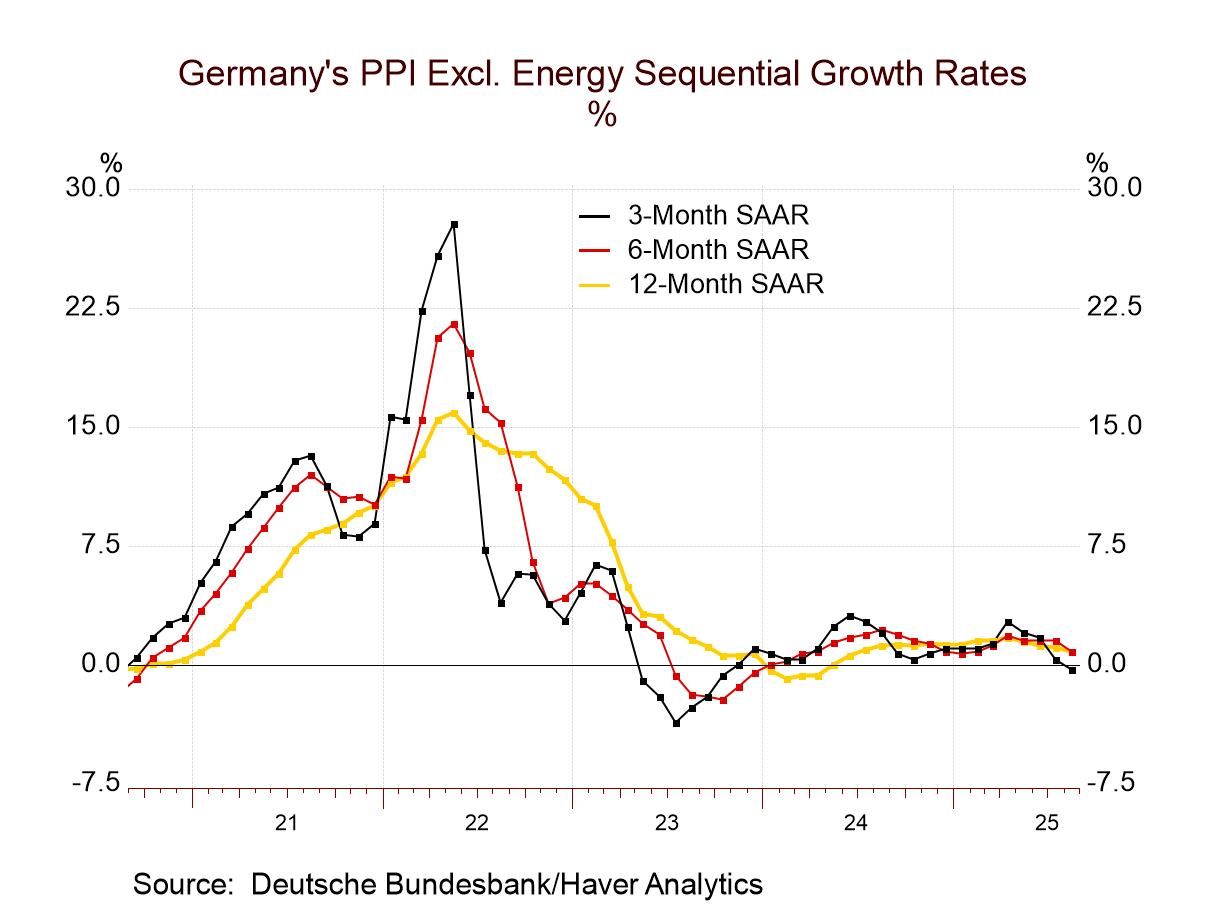

The German PPI report showed a drop of 0.5% in the August headline, continuing a string of inflation data on the producer price front that is laying a solid disinflationary trend for the German economy. The PPI rose by 0.1% in July and in June. Sequentially the PPI falls 2.2% over 12 months, falls at 3.9% annual rate over six months, and falls at a 1.3% annual rate over three months, an impressive record of inflation discipline at a time that consumer inflation has been running hot globally.

Germany's PPI excluding energy also fell in August, dropping by 0.2% on the month after being flat in July and rising 0.1% in June. The PPI excluding energy for Germany rises 0.8% over 12 months, rises at a 0.8% annual rate over six months, and falls at a 0.3% annual rate over three months. The inflation discipline extends past energy; it is not simply disciplined energy prices although that has been part of the story.

Sectoral German PPI data are not seasonally adjusted making their sequential patterns a little bit less dependable. However, sequentially German consumer prices show inflation has been dropping, the same is true for investment goods, whereas for intermediate goods, not only is inflation dropping but prices are dropping too; inflation is negative over 12 months, six months and three months with the 3-month drop in intermediate prices at a -3.4% annual rate.

The behavior of producer prices compares to modest results on the CPI front where, sequentially, the German CPI rose 2.3% over 12 months, at a 1.8% pace over six months, and then at a 2% pace over three months, all well-contained changes. The CPI excluding energy rose by 2.6% over 12 months, 2.5% over six months, and 2.4% over three months showing a very slight deceleration with inflation looking still very sticky at about 1/2 of a percentage point above what is the target pace set by the ECB for the European Monetary Union as a whole.

Global| Sep 18 2025

Global| Sep 18 2025Charts of the Week: Faith in the Fed, Faith in Fiber

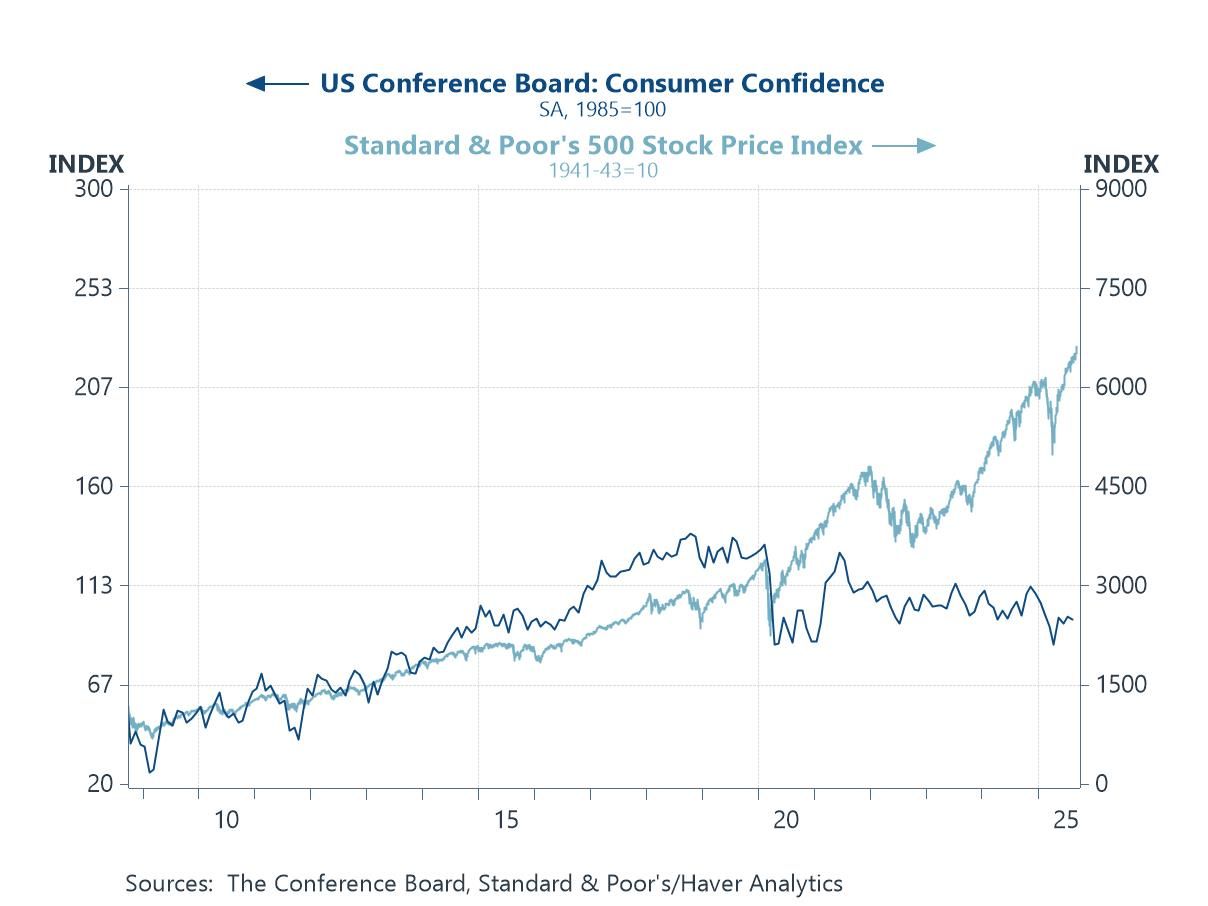

Global equity markets have remained near record highs over the past few days following the Fed’s 25bp cut on Wednesday, and which investors have seen as a key prop even without a full dovish pivot. AI optimism is also arguably doing some heavy lifting: markets are pricing a step-change in economy-wide productivity and margins from AI adoption, lifting multiples—especially among AI-exposed companies. However, some of this week’s charts frame the hurdles those hopes must clear: US consumer confidence remains subdued even as equities rise (chart 1); the Fed’s forward path is potentially becoming more politicised and inflation expectations have not softened in line with oil (chart 2); economists’ 2025 profit growth forecasts, in the meantime, have been marked lower and dispersion is wide, leaving valuations reliant on an AI-led earnings re-acceleration (chart 3). Elsewhere in Asia, earlier and ongoing easing underscores weak domestic demand and tariff risks rather than robust momentum (chart 4). Commodity dynamics could help at the margin—food prices have eased on better harvests and smoother supply chains (chart 5). Finally, and ahead of this week’s BoE decision in the UK, elevated services inflation tied to still-lofty pay growth is complicating the scope for further policy easing. In sum, the equity narrative arguably leans heavily on AI delivering tangible, near-term earnings power while policy remains credible and inflation contained; disappointment on any front in other words could challenge today’s valuations.

by:Andrew Cates

|in:Economy in Brief

- Current General Activity Index improves to highest level since January.

- Inflation reading declines to seven-month low.

- Future General Activity Index continues upward movement.

by:Tom Moeller

|in:Economy in Brief

- Initial claims declined 33,000 in latest week.

- Continuing claims were down slightly.

- Insured unemployment rate holds steady.

- of2736Go to 75 page