- The headline index jumped nearly 20 points, led by strong performances by both orders and shipments.

- However, ISM-adjusted composite slipped a bit, indicating that the jump in the headline index was not widely supported by the components.

- Delivery times shortened markedly while both prices paid and prices received indexes posted significant gains.

USA| Jul 17 2025

USA| Jul 17 2025U.S. Philly Fed Manufacturing Index Jumps in July

by:Sandy Batten

|in:Economy in Brief

USA| Jul 17 2025

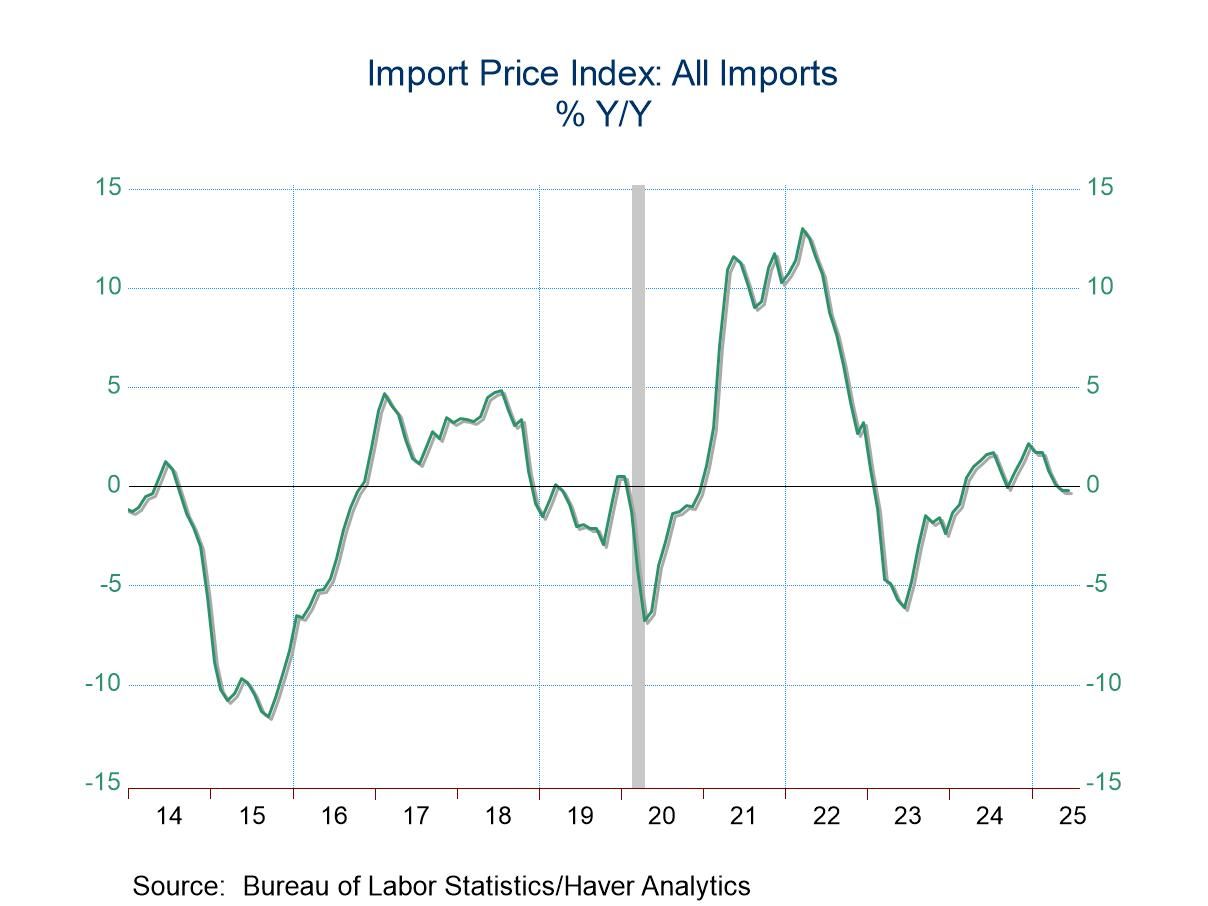

USA| Jul 17 2025U.S. Import Prices Edged Up and Export Prices Rebounded in June

- Import prices edged up in June from May but fell from a year ago.

- Higher prices for nonfuel imports more than offset lower prices for fuel imports in June.

- Export prices jumped more than expected, nearly reversing May’s decline.

- Prices rose for both agricultural and nonagricultural exports.

by:Sandy Batten

|in:Economy in Brief

USA| Jul 17 2025

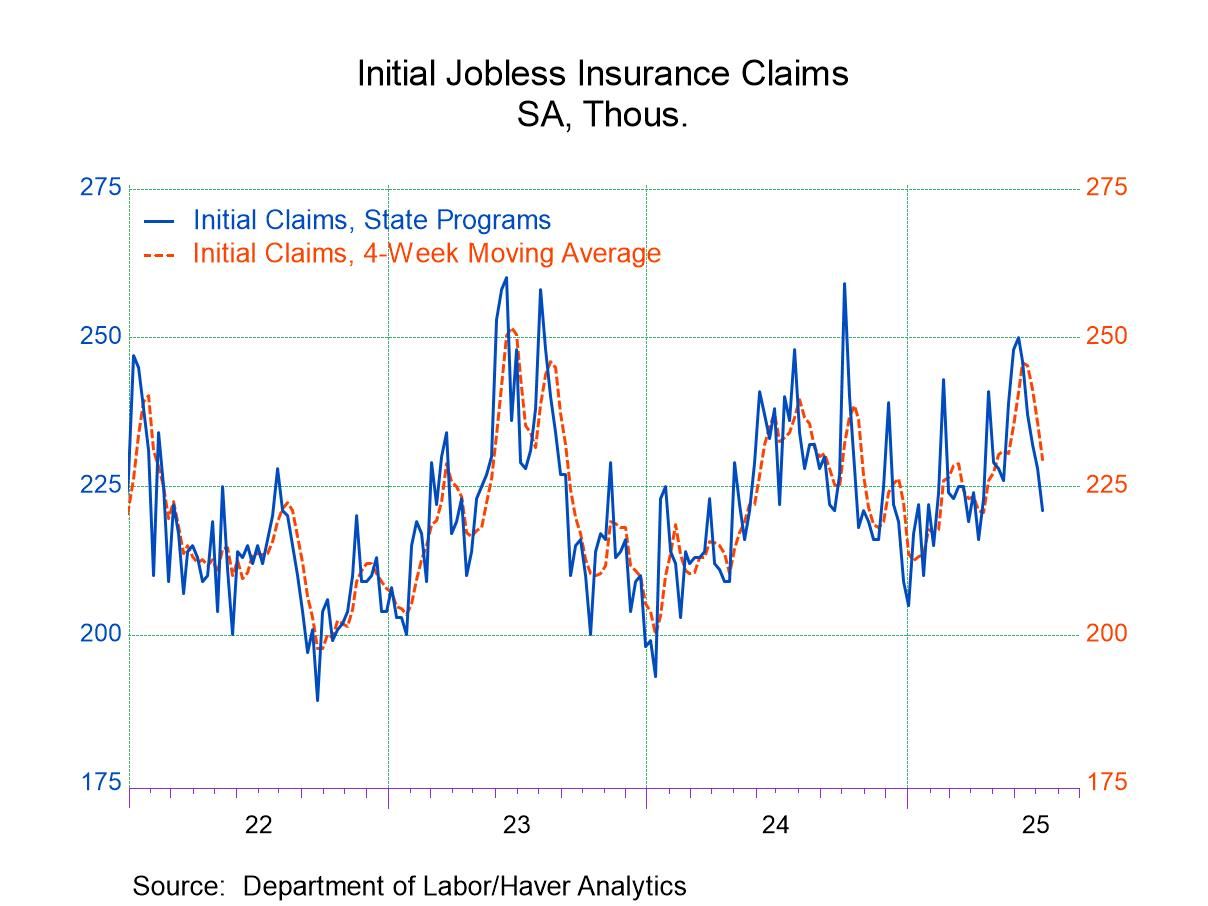

USA| Jul 17 2025U.S. Initial Unemployment Insurance Claims Fell in Latest Week

- Initial claims have declined for five consecutive weeks.

- Continuing claims rose slightly in the July 5 week.

- Insured unemployment rate was unchanged for the sixth consecutive week.

Australia| Jul 17 2025

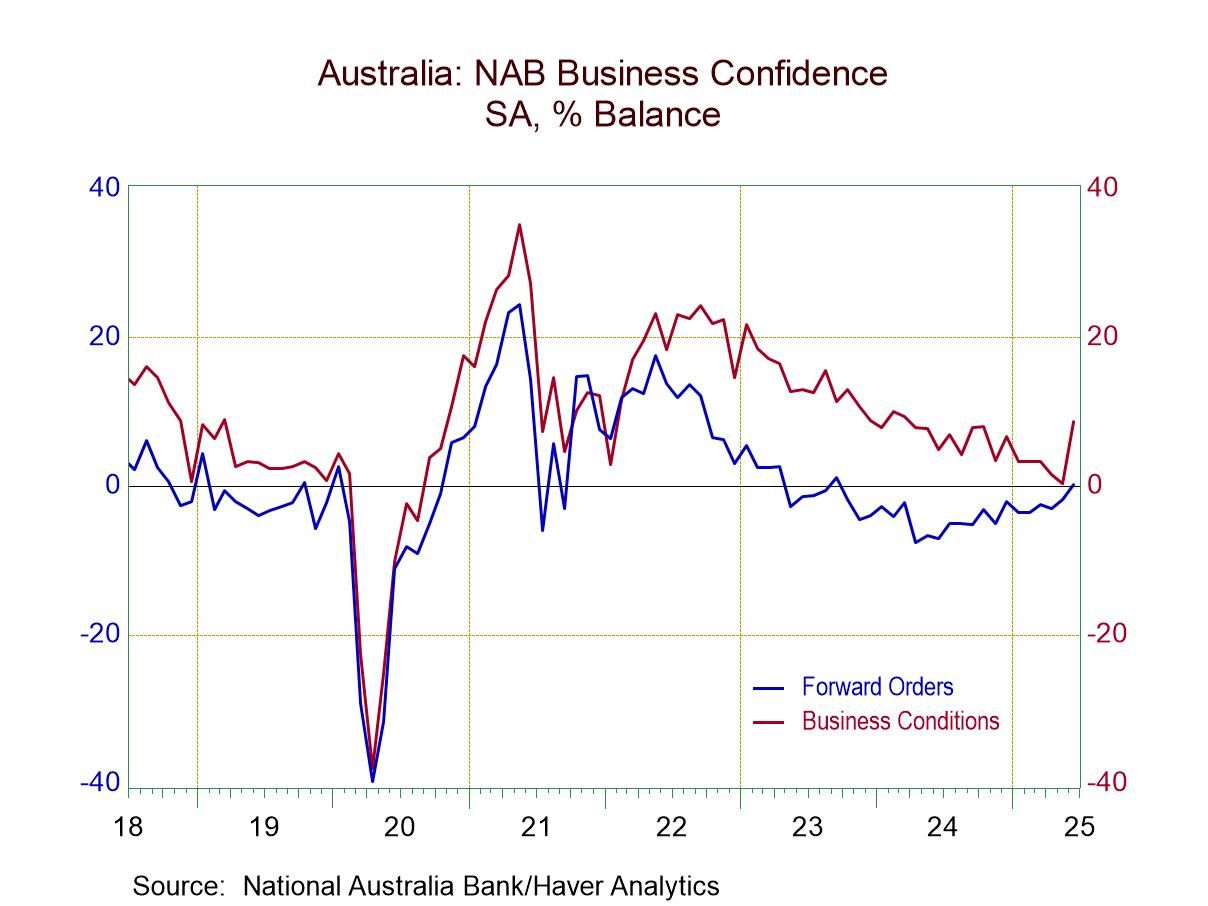

Australia| Jul 17 2025Aussie Business Confidence -National Australia Bank Survey

The National Australia Bank (NAB) survey for June shows a jump in Australia’s business confidence to 5.1 from 2.2 in May and those compared to a reading of -0.7 in April. The sequential averages show a steady improvement from a 12-month average of 0.2 to a six-month average of 1.3 and to a three-month average of 2.2. The monthly May reading is at 2.2. With the June reading moving up to 5.1, it looks like this progression toward improvement remains in train.

Smoothed assessments Smoothing out the monthly data shows that the three-month smoothing operation switches the progression from 12-months to six-months to three-months to reveal improvement that has stalled out. Looking at 12-month averages, there's an improvement over six months compared to 12-months, and then a slight set-back over three months.

Components The components over three months show improvement in train for about half of the categories, compared to 43.8% improving over six months and 25% improving over 12 months. The sense of improvement across categories has been broadening over the more recent periods.

Standings Percentile standings on the data back to 2002 show above-median standings in seven of the thirteen survey categories. Over this period, business confidence itself ranks slightly below its median with a 49.5 percentile standing; the median occurs at a standing of 50-percentile. The index of business confidence is currently close to its median on this, but slightly below it. However, the rankings for the three-month moving average and the 12-month moving average both are considerably lower, indicating that much of the improvement that we see in the Australian index is relatively recent.

Summing up Australia remains caught up in tariff negotiations with the United States along with every other country, a factor that extends uncertainty and could be holding back progress in the economy. However, the current survey suggests that progress is in train, nonetheless.

USA| Jul 16 2025

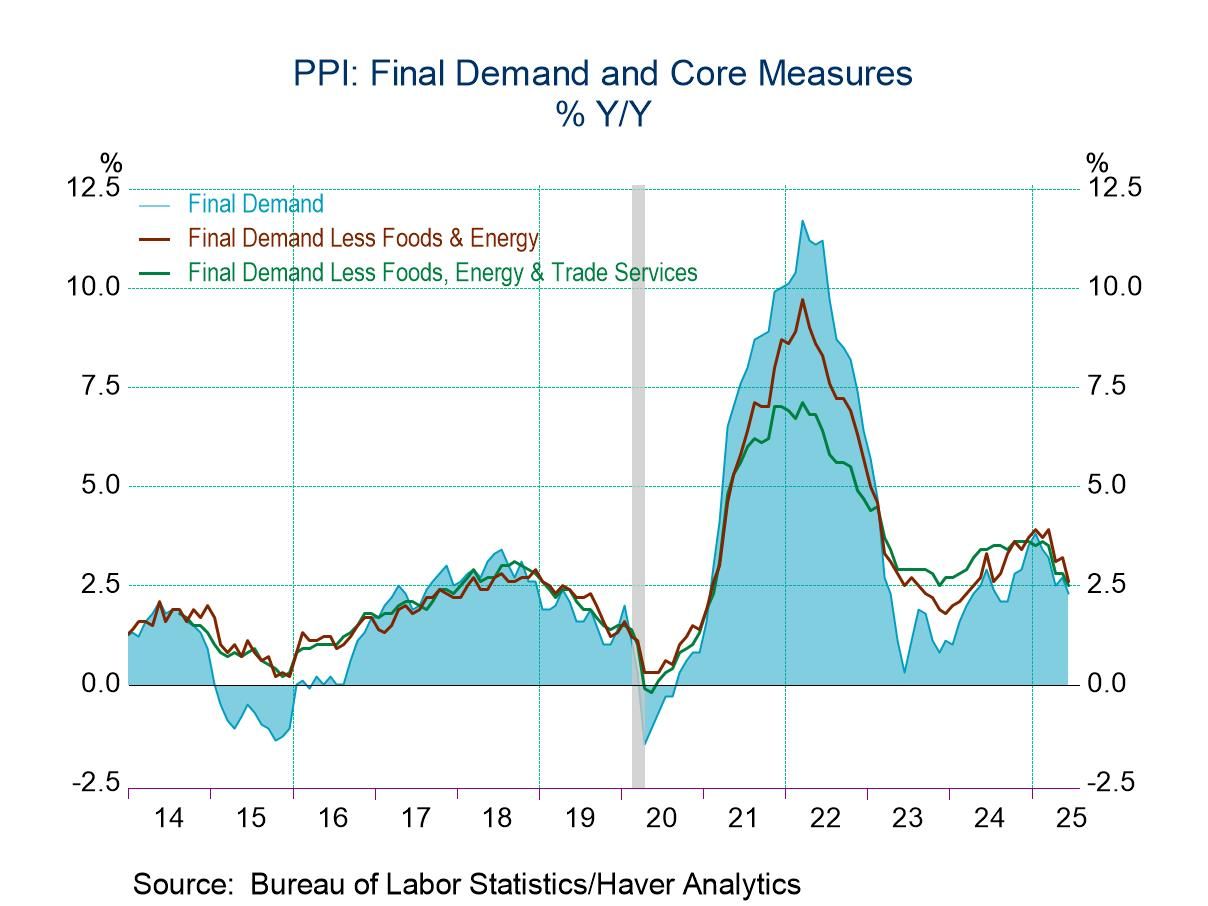

USA| Jul 16 2025U.S. Producer Price & Core Price Indexes Hold Steady in June

- Unchanged monthly levels extend weakness earlier this year.

- Core price gain slows y/y.

- Final demand price index is steady; services prices decline.

by:Tom Moeller

|in:Economy in Brief

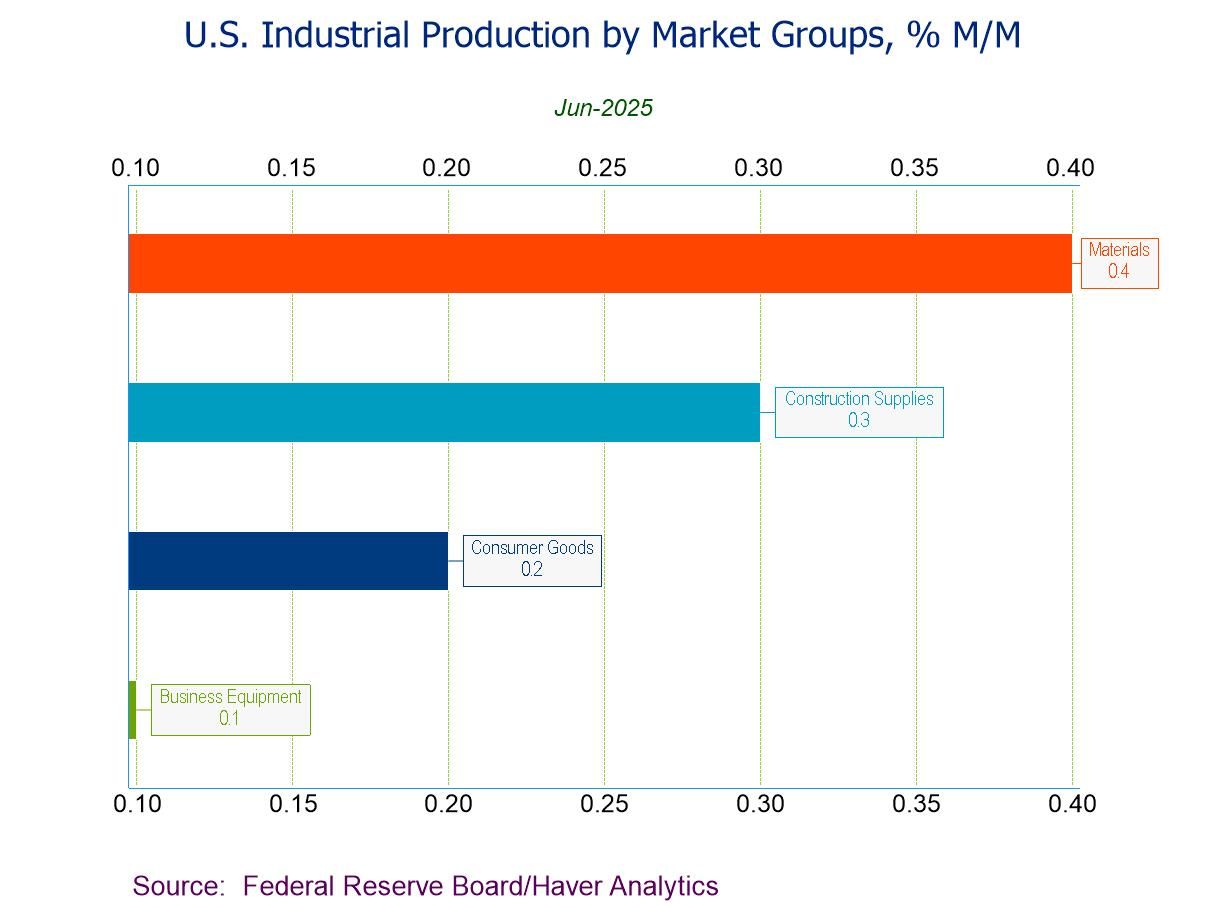

- June IP +0.3% (+0.7% y/y), led by a 2.8% rebound in utilities output.

- June IP Index at the highest level since Dec. ’18.

- Mfg. IP +0.1%, w/ durables unchanged and nondurables up 0.3%.

- Mining activity -0.3%, the second m/m fall in three months.

- Key categories in market groups all increase.

- Capacity utilization up 0.1%pt. to 77.6%; mfg. capacity utilization up 0.1%pt. to a 3-month-high 76.9%.

USA| Jul 16 2025

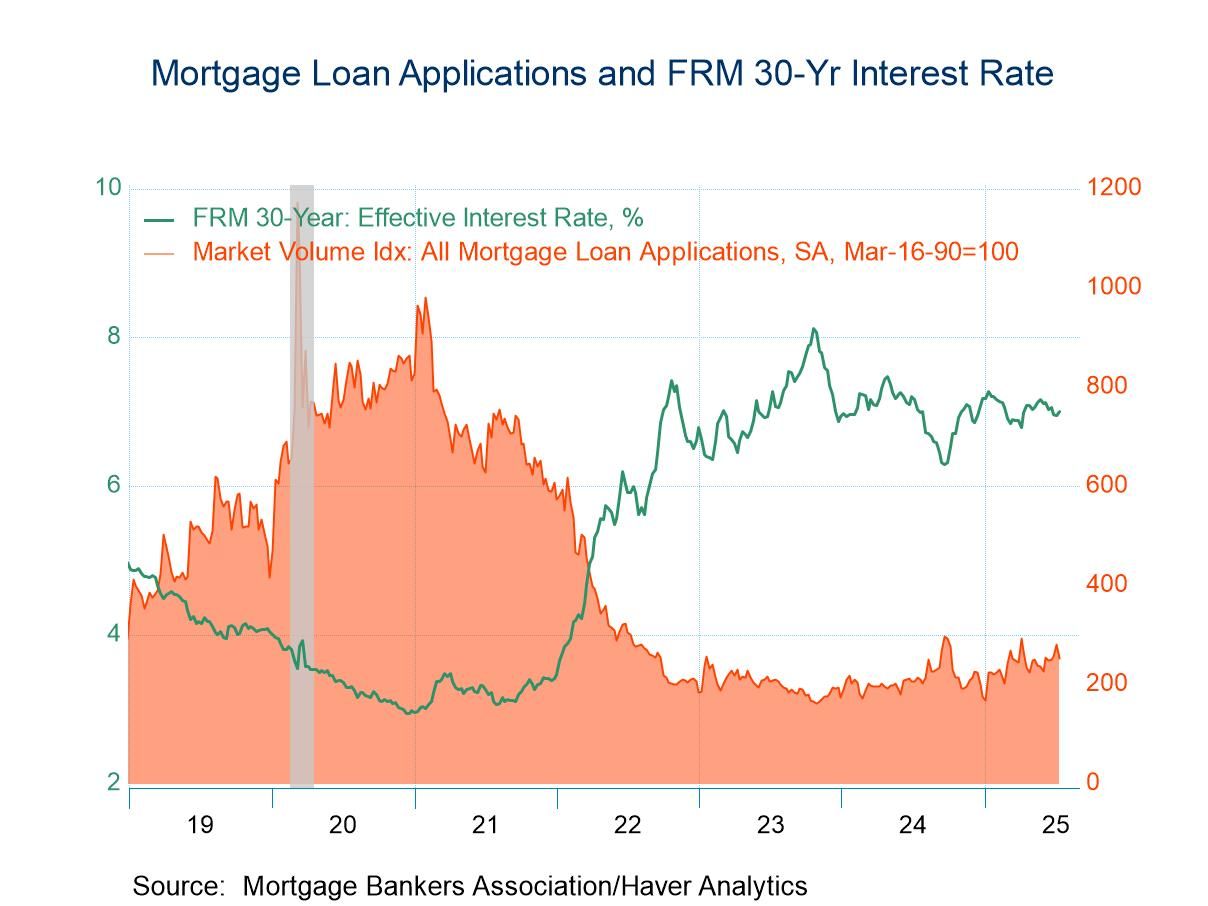

USA| Jul 16 2025U.S. Mortgage Applications Dropped 10.0% in the Latest Week

- Both purchase applications and refinancing loan applications fell in July 11 week.

- Effective interest rate on 30-year fixed-rate loans rose to 7.0%.

- Average loan size declines for the fourth time in five weeks.

United Kingdom| Jul 16 2025

United Kingdom| Jul 16 2025U.K. CPIH Inflation Runs Hot

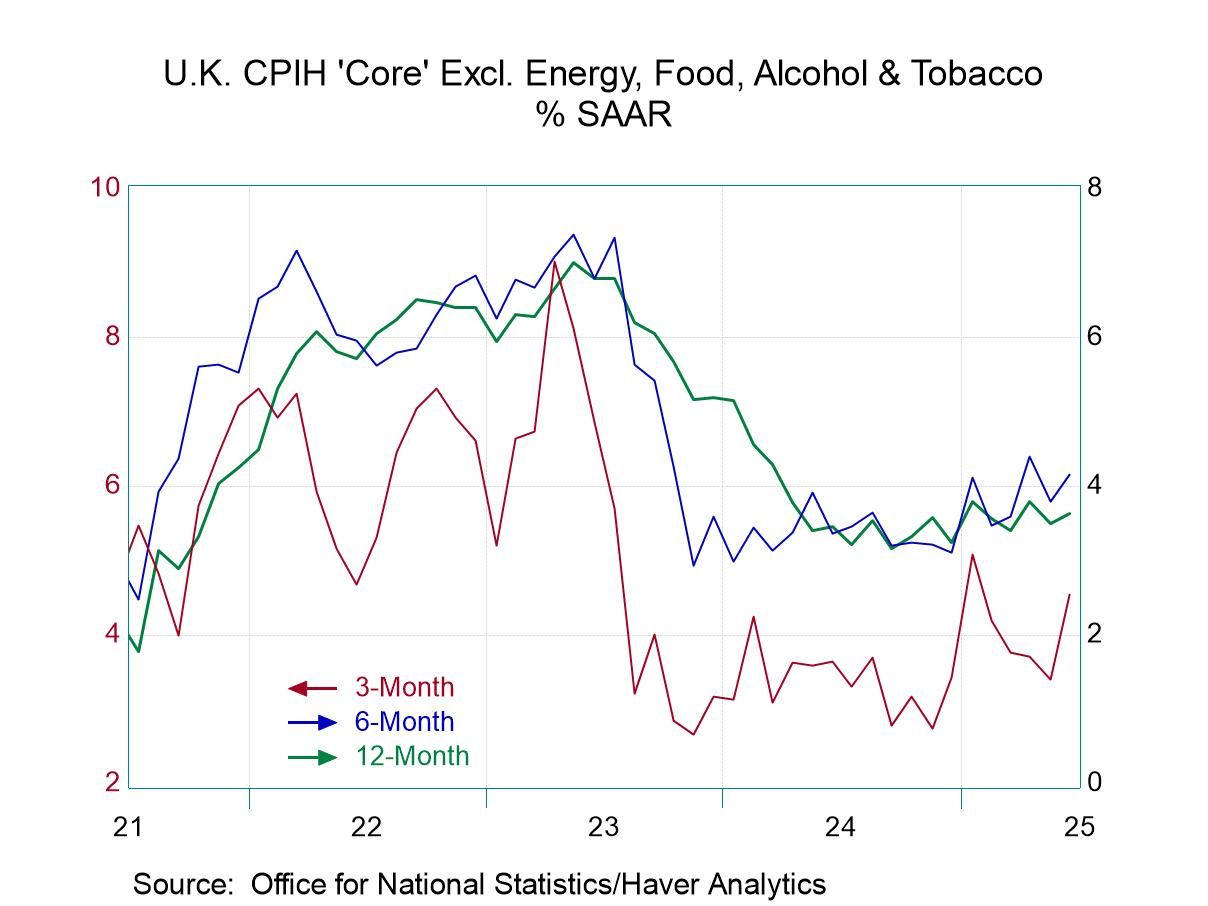

Inflation in the United Kingdom is still running hot in June. The CPIH rose by 0.4% in the month with its core rate that excludes energy, food, alcoholic beverages & tobacco also rising 0.4% month-to-month. In both cases, these increases compare to a rise of 0.1% in May. On that perspective, the two-month trend is somewhat muted. However, in April the CPIH headline rose by 0.6% and the core rose by 0.4%, so the U.K. finds itself in another period of excess inflation.

Sequential inflation The sequential inflation rate from 12-months to six-months to three-months shows the headline at 4.1% over 12 months, 4.2% over six months and 4.3% over three months, a very slight acceleration, but clearly inflation that is over 2 percentage points above the target set by the Bank of England across the entire span. The core rate for the CPIH is up 4.3% over 12 months, up at a 4.4% annual rate over six months and looks slightly muted at 4.2% over three months. Again, we are looking at a solid inflation overshoot that is more than 2 percentage points above the target set by the Bank of England.

Inflation breadth In the month of June, inflation accelerated in 45% of the categories, the same proportion as in May; however, in April acceleration occurred in 54% of the categories. These sequential data show that over three months inflation in the U.K. accelerated across 54% of the categories, the same proportion as over six months although both of those marks were below the 63% acceleration breadth logged over 12 months. The data clearly show that there isn't any deceleration to any great extent in play over any of these horizons and that the monthly data offer only a modicum of solace for June and May.

The far-right hand column evaluates current inflation rates year-over-year compared to where they have been since January 2000, monthly. The comparison is a ranked percentage of the current inflation rate vs. this history. For example, the current CPIH 12-month inflation rate of 4.1% sits at the 88.6 percentile of its historic queue of data. This tells us that inflation has been this high or higher, less than 12% of the time over this period, clearly marking the 4.1% growth rate as high and as substantial by historic experience. The CPIH core has a slightly higher standing and it's 89th percentile. Looking across the components, all but two have rankings over this 50%. Rankings that are above 50% place them above their medians for the period. The exceptions here, are a 26.5 percentile standing for restaurants & hotels inflation where prices are running at 2.6%, and transportation where prices are running at 1.6%. Furniture, household equipment & maintenance prices have a 56.2 percentile standing, only marginally above the category’s historic median. After that, there's only one category in its 60th percentile, two categories in their 70th percentile and the rest are higher.

Summing up Needless to say, the U.K. has an entrenched inflation problem. It's lodged in the headline; it's lodged in the core; it's lodged across most of the commodity categories! The Bank of England simply has work to do and there isn't much evidence that the BOE is making any progress; in fact, the trends seem to suggest that there may be much more work to do.

- of2736Go to 95 page