- Light truck sales decline while auto purchases improve.

- Domestic and import sales decline.

- Imports' market share steadies.

USA| Sep 03 2025

USA| Sep 03 2025U.S. Light Vehicle Sales Ease in August

by:Tom Moeller

|in:Economy in Brief

USA| Sep 03 2025

USA| Sep 03 2025U.S. JOLTS – Job Openings Decline While Hiring Improves in July

- Job openings fall for second straight month.

- Hiring improves after two consecutive months of sharp decline.

- Separations fall, quits ease but layoffs rise slightly.

by:Tom Moeller

|in:Economy in Brief

- Headline: -1.3% m/m; +1.6% y/y, the smallest y/y gain in three months.

- Durable goods orders (-2.8%) down, but nondurable goods orders (+0.3%) and shipments (+0.9%) both up three straight months.

- Transportation equipt. orders -9.5% m/m, w/ a 32.7% drop in nondefense aircraft & parts orders.

- Unfilled orders unchanged after two successive m/m increases.

- Inventories +0.3%, the third consecutive m/m rise.

USA| Sep 03 2025

USA| Sep 03 2025U.S. Gasoline & Crude Oil Prices Rise Last Week

- Gasoline prices increase to highest level in four weeks.

- Crude oil prices recover after earlier declines.

- Natural gas prices at early-June low.

by:Tom Moeller

|in:Economy in Brief

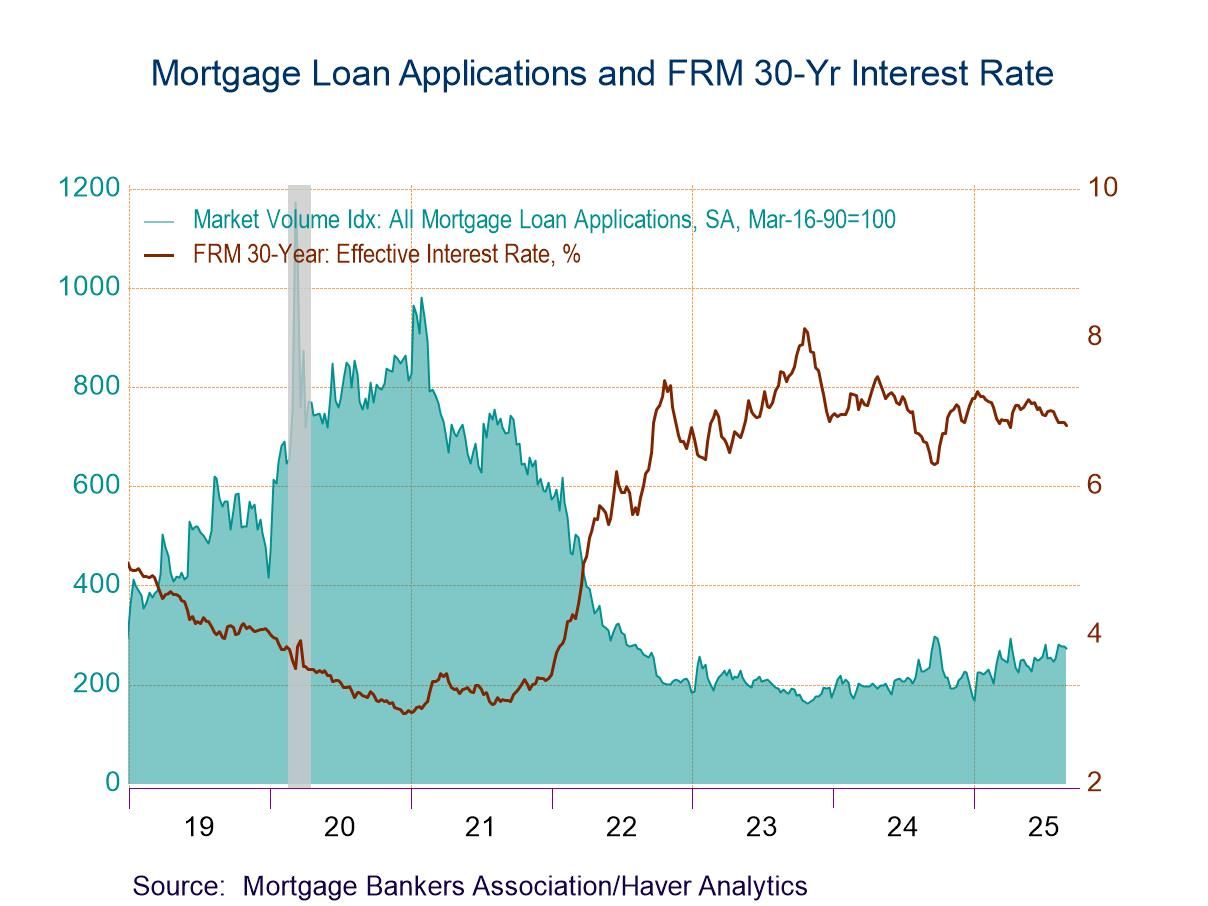

USA| Sep 03 2025

USA| Sep 03 2025U.S. Mortgage Applications Declined in Latest Week

- Purchase applications dropped while loan refinancing edged up.

- Fixed-interest rate on 30-year loan holds at a 4-month low.

- Average loan size edged up.

Global| Sep 03 2025

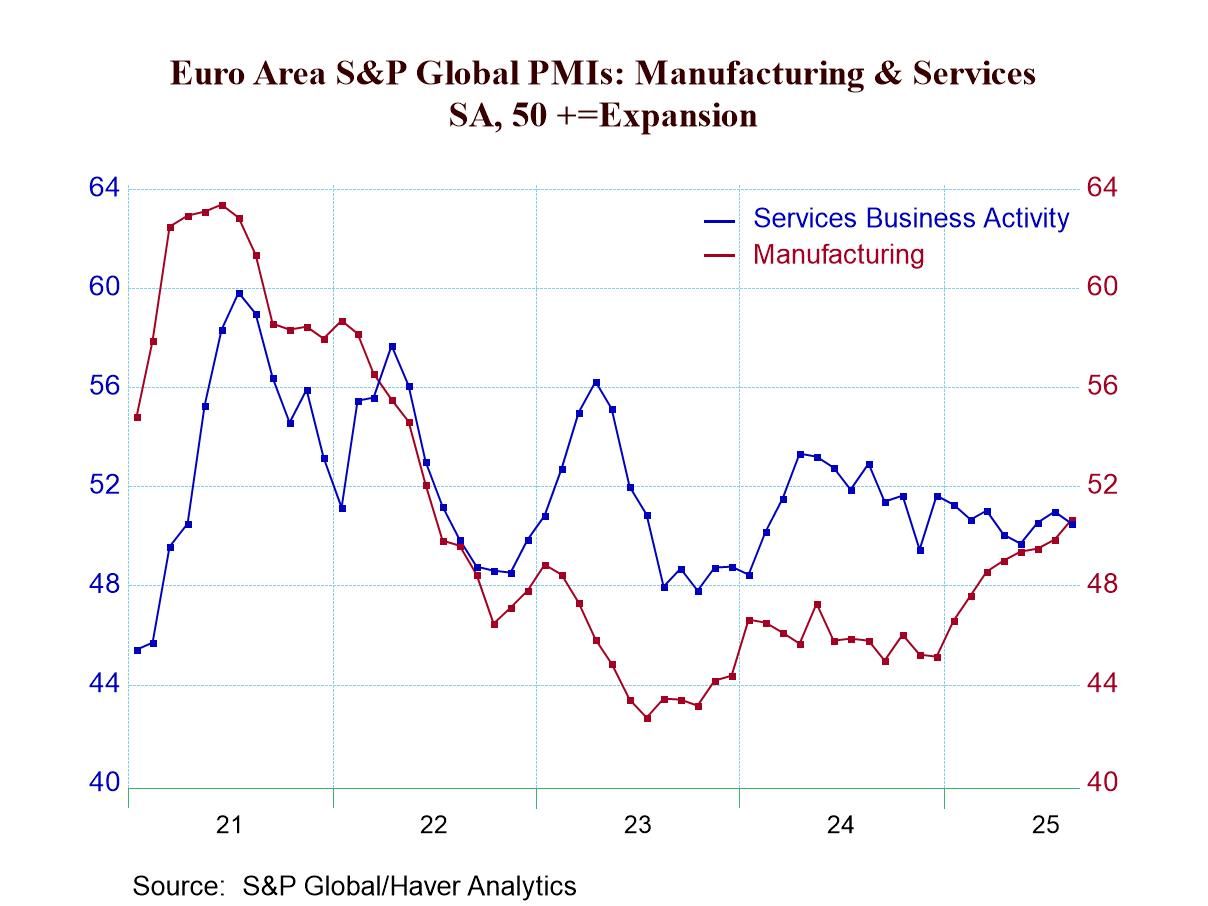

Global| Sep 03 2025S&P Composite PMIs Improve in August

The S&P composite PMIs in August have advanced broadly with only four of 25 reporters showing weaker conditions in August compared to July. In July 13 of these same reporters showed worsening conditions and in June 12 reporters showed worsening conditions. August is a marked turnaround for this survey. One caveat is that the U.S .data in this report continued to use the preliminary services estimate because the final U.S. estimate is not yet available.

Over three months compared to six months, 9 of 25 reporters show worsening conditions. Over six months compared to 12 months, 12 of 25 reporters showed worsening conditions. Over 12 months compared to a year ago, 15 reporters out of 25 showed worsening conditions. There has been a progression in terms of the breadth for reporting countries that are showing improvement in addition the overall average. It has improved slightly from 51.7 over 6 and 12 months to 51.9 over 3 months. The medians have improved from 51.1 over 12 months to 51.5 over 6 months to 51.6 over 3 months, a slightly clearer progression toward better results. Still, both of them are on fairly thin margins of improvement. However, June to August the averages and medians show a little bit more movement and a little more progression to better readings.

The statistic that is perhaps most encouraging is the one about the percentage of reporters that are weaker in August; only 16 were weaker compared to July; in July 52% were weaker compared to June, but in June 48% were weaker compared to May. Looking at the broader progressive period, 39.1% are weaker over 3 months, 52.2% are weaker over 6 months compared to 39.1% weaker over 12 months. The proportion of reporters weakening over these horizons is moderate on the order of 40% to 50%- tending to readings below 50%.

The queue percentile standings show only 8 reporters out of 25 have standings below their median since January 2021.

The chart on top depicts separately the services business activity index for the euro area versus the euro area manufacturing PMI. While the services readings have been relatively stable - perhaps trending slightly to weakness from earlier in the year - manufacturing PMIs have been improving consistently and strongly. At first it was thought that this was manufacturing activity that was ramping up to try to create output to export before U.S. tariffs went into effect, but since the tariff deadline has come and gone, manufacturing has continued to stay strong and to further strengthen. This is an unexpected and impressive trend.

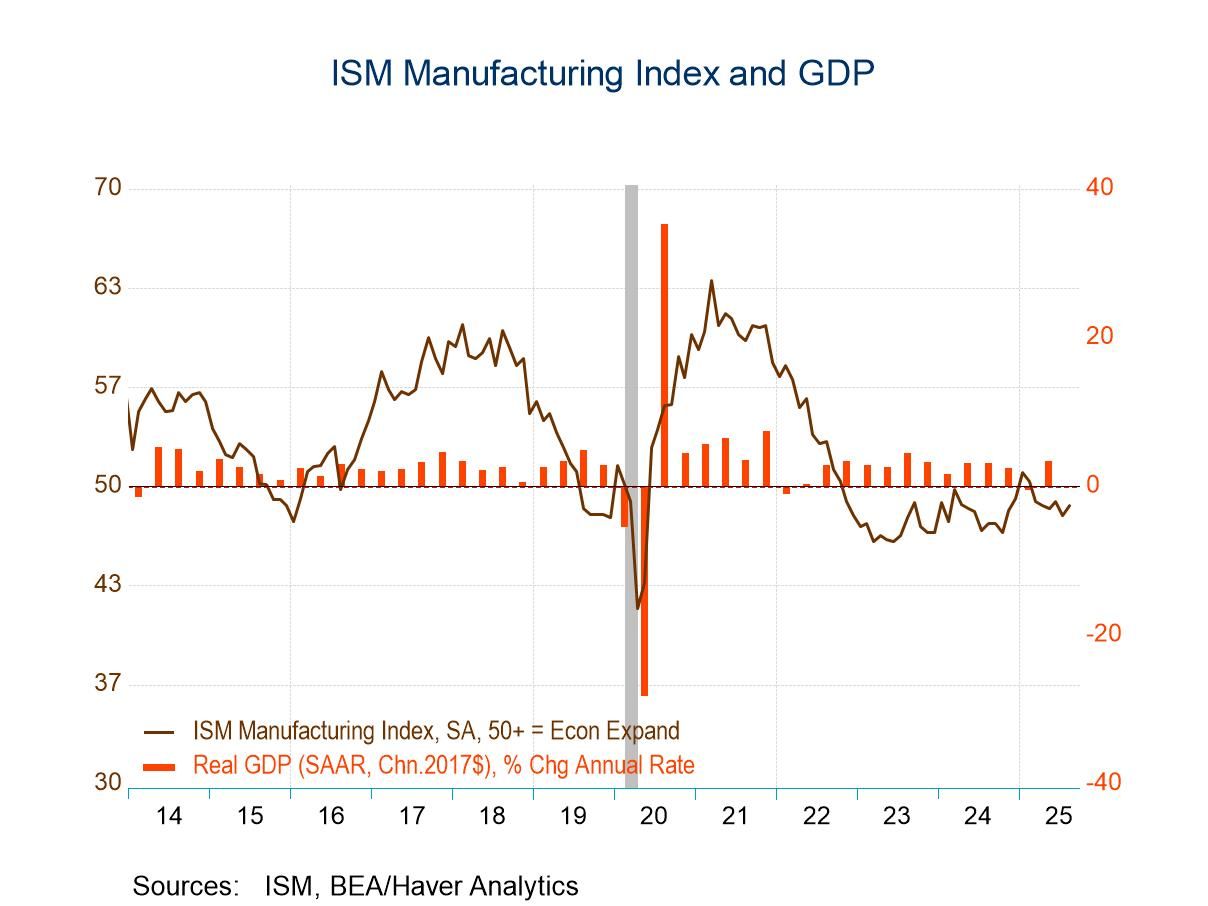

USA| Sep 02 2025

USA| Sep 02 2025U.S. ISM Manufacturing PMI Increases in August; Prices Ease

- Improvement fails to recover all of July decline.

- New orders gain offsets production decline.

- Price index falls to six-month low.

by:Tom Moeller

|in:Economy in Brief

USA| Sep 02 2025

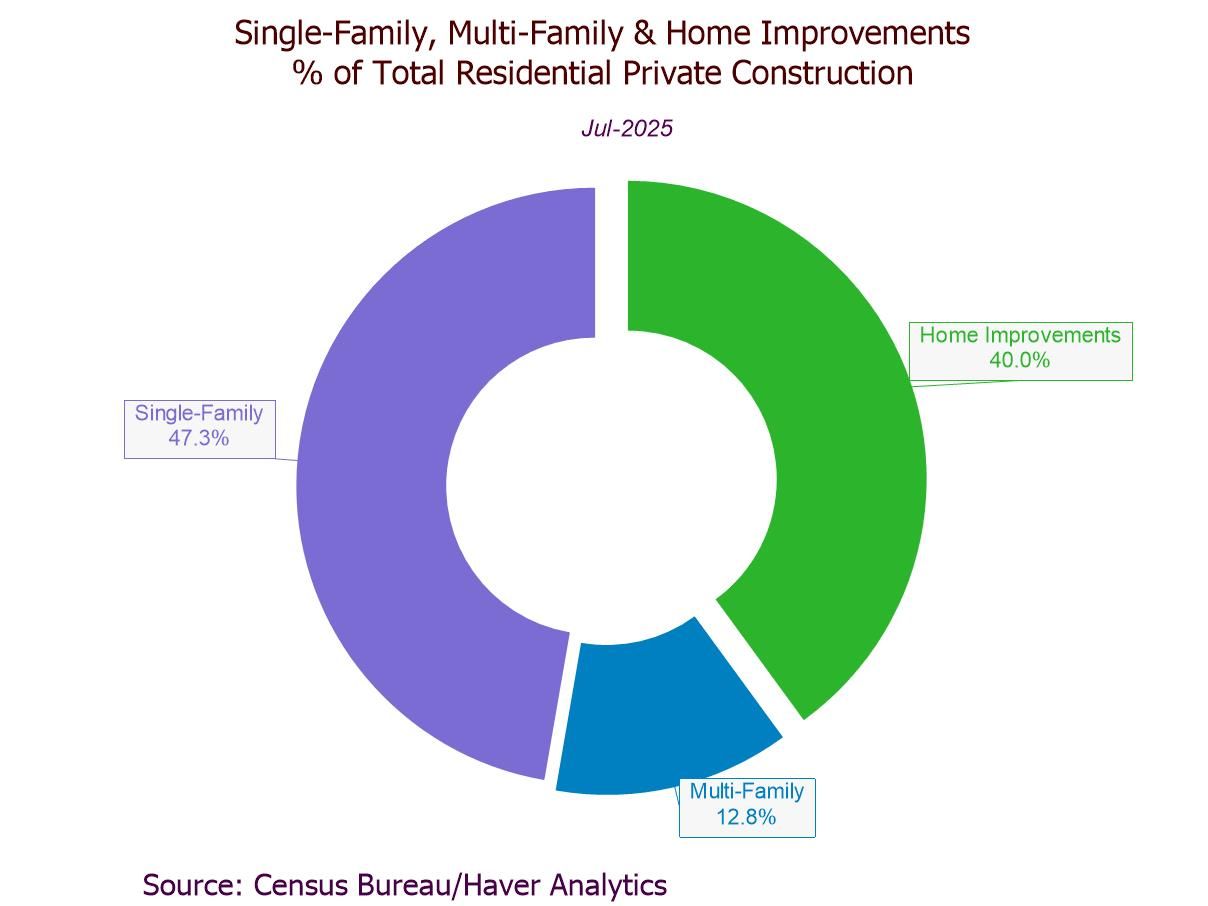

USA| Sep 02 2025U.S. Construction Spending Eases in July

- Headline: -0.1% m/m, the third straight m/m fall; -2.8% y/y, the sixth straight y/y slide.

- Residential private construction +0.1% m/m, up for the first time since December.

- Nonresidential private construction -0.5% m/m, the third consecutive m/m decline.

- Public sector construction +0.3% m/m, led by a 1.8% rebound in residential public building.

- of2693Go to 38 page