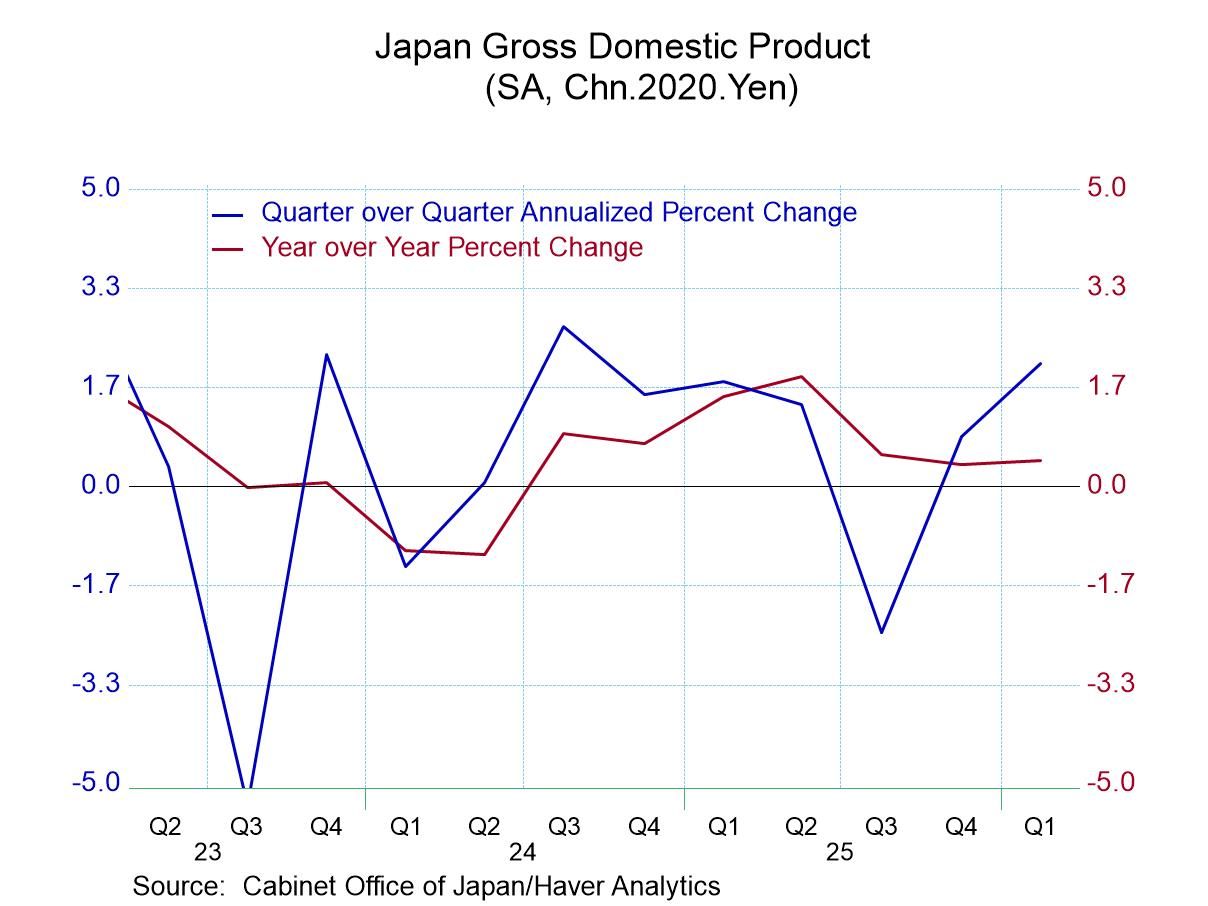

Japan’s GDP rose 2.1% annualized in 2026-Q1. The gain beat expectations for the quarter. The 2.1% rise was the largest gain since a 2.7% rise in 2024-Q3. However, it still leaves the year-on-year gain for GDP at 0.4%, the same as for 2025-Q4. And these are the weakest growth rates since Q1 and Q2 of 2024 when Japan’s GDP was declining.

Private consumption in 2026-Q1 rose by 1.1% quarterly at an annualized rate, its strongest gain in a year. Still, the year-on-year rise in private consumption slowed to 1% from 1.4% in 2025 Q4. Growth in private consumption on a year-on-year basis is the weakest it has been since 2024-Q4.

Despite some signs of GDP/Consumption stirring, the quarterly performance is not enough to boost the year-on-year growth rates to a position of strength, let alone firmness. Japan has simply been struggling for a while. And now with inflation bulging the BoJ has been super careful to move rates exceptionally slowly so that real interest rates in Japan remain exceptionally low (negative, still) and the prospect of rate normalization in Japan still seems to be a distant dream.

New PM Sanae Takaichi called her snap election and improved her grip on government and is still looking to stimulate the economy, but Japan’s fiscal position is now so precarious that even the usual incantation that Japan owns most of its debt to itself (its own residents) has not been reassuring. Japan has become wary of is debt-to-GDP ratio. The time for a fiscal surge has passed and there is talk instead of a new industrialization policy to try to stimulate the economy within the realm of current spending trends by offering improved incentives for growth.

Capital formation in GDP grew by 2.1% in 2026-Q1, a down shift for 2025-Q4, but capital spending is in a period of some volatility. The year-on-year gains show a step up in Q1 spending to a pace of 1.5% from 1.2% in the previous quarter. The five-year growth rate for capital spending is only 0.8% per year. Still there is not much here to build economic revival on.

Plant and equipment spending has weakened in Q1, showing an annualized Q/Q gain of 1.1% and that compares to five-year annualized growth of 1.8%. Year-on-year plant and equipment growth is at 2.8%.

Spending on housing turned sharply higher in Q4 with a smaller continued gain Q/Q in 2026-Q1. Still, after some considerable weakness quarterly, the year-on-year gain in housing spending in Japan in 2026-Q1 is -3.1% marking the third quarter in a row of declining spending on housing year-over-year.

Net exports in Japan turned sharply higher in 2026-Q1 and year-on-year the change in the GDP-net exports balance swung from negative to positive. The annual improvement in the net export position is still only half of what it had been over the last five years. Export growth spiked while import growth stepped up in 2025-Q1. Exports and imports over the past year both growth more slowly than their 5-year averages.

Domestic demand picked up a bit Q/Q in 2026, but the year-on-year growth slipped to 0.3% compared to a gain of 1.2% in the previous quarter.

Japanese officials are engaged in active market talk to try to restrain further slippage in the yen. Markets buzz with rumors of intervention that has not happened for over a month. Japan’s decision on interest rate is also caught up in its concerns about the yen. Meanwhile, as Japan imports all its fuel and rising energy prices are a concern in Japan. Yet the concern is about the future more than anything else since Japan tends to sign long-dated energy contracts and likely has locked up its oil price costs for this year. Still, the ongoing pressure has put conditions in doubt for the year ahead.

On balance Japan growth in 2026-Q1 was somewhat better than expected but it has done nothing to assuage concerns about the way forward. Ongoing inflation and a reticence to hike rates to address inflation continue to stalk the policy outlook as PM Takaichi looks for a way out of Japan’s weak growth trap.

Asia

Asia