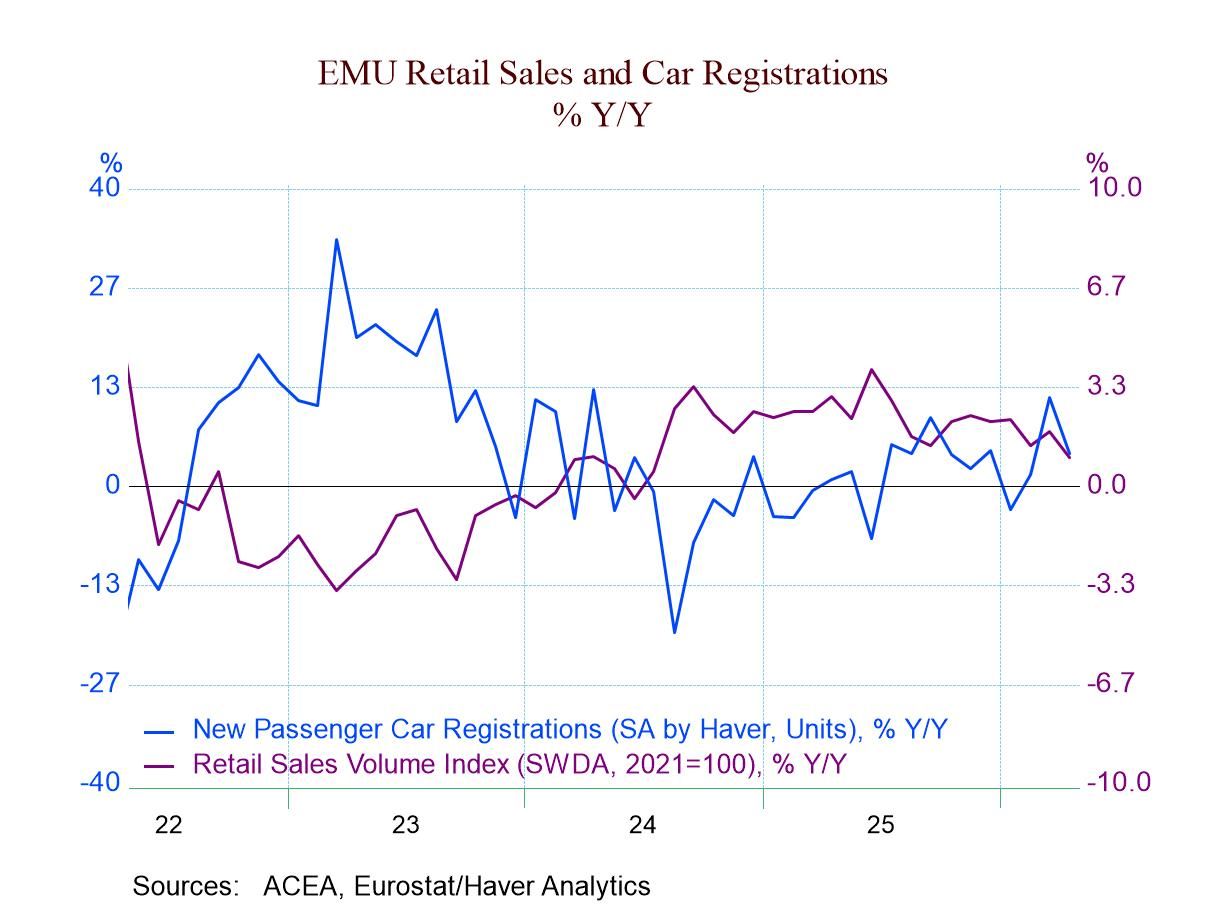

Retail sales in the euro area declined in volume terms in April, falling 0.4% on the month after rising 0.8% in March and falling 0.5% in February. Food and beverage volume recovered to post an expansion after two monthly declines.

Sales trends slip: However, the headline for retail volume growth shows that there has been steady slippage, with growth over 12 months weaker than it was over the previous 12 months, growth over six months at a weaker pace than it was over 12 months, and growth over three months posting an outright decline compared to a gain over six months. The highlighted red background in the table shows this string of continuous slowing that marks decelerating retail spending in the euro area as of April. In the quarter to date, retail sales volumes are declining at a 0.2% annual rate—a very slight contraction but a net reduction in sales volume, nonetheless, to start the second quarter.

Contrarian strength in vehicle demand: Motor vehicle registrations pulled back in April after some strong gains in earlier months. Motor vehicle registrations are accelerating as the growth rate rises from 12 months to six months to three months; growth actually explodes over three months, rising at a 52.4% annualized rate. With this strength, naturally, motor vehicle registrations are logging strong growth at the beginning of this new quarter, rising at a 33.6% annual rate.

Despite the strength in motor vehicle registrations, registrations are still a lot lower in comparison to January 2020. They have averaged a decline of 1.2% per year over this period. Since January 2020, just before COVID struck, retail sales in the euro area have risen by 6.7%, implying an average annual growth rate of 1% per year. This has generally been a lethargic period for retail sales.

Sales trends by country Looking at the individual countries in the table, we chronicle developments for EMU members Germany and the Netherlands, EU member Denmark, and Northern European countries Norway and Sweden, plus former EU member the United Kingdom. We see that all of these countries have had a long period of weak growth going back to January 2020. Among these countries, only Denmark and the Netherlands have averaged retail volume growth of over 1% for this date-span; Denmark averages 1.5% per year, and the Netherlands averages 1.3%. Sweden and Norway’s trends average 0.8% and 0.7% growth per year back to January 2020. Germany posted a compounded annual increase of only 0.6% annually, while in the U.K., in the wake of the problems that COVID and Brexit created, saw its retail sales volumes decline annually by 0.4%, marking a 2.2 percentage point decline in retail sales since January 2020. It has been a weak environment for retailing.

Recent sales performance: Up-to-date observations for April show declines in retail sales volume in Germany, Denmark, and the U.K., with flat sales in Sweden. Norway logs an increase of 0.3% month-to-month, and the Netherlands logs an increase of 1.6% month-to-month. The sequential data, looking at sales over 12 months to six months to three months, largely points to a continuation of this period of lethargic sales. Germany, the U.K., and Norway each are posting a sequential deceleration, as the rate of sales slows over progressively shorter time periods. Denmark and the Netherlands have somewhat erratic performance on retail sales, with no clear trends. Sweden stands alone as the only country with retail sales clearly accelerating, rising 4.2% at an annual rate over 12 months, at a 4.4% annual rate over six months, and at a 5.8% annual rate over three months.

Challenging outlook The retail environment remains challenging in Europe. Oil prices are rising; the European Central Bank is expected to take steps to deal with excessive inflation and rising oil prices with at least one rate hike. The war in Ukraine remains hot; the war in the Middle East may be cooling down, but the Strait of Hormuz is still not open for business. The global economy continues to face significant challenges.

Global

Global