Global

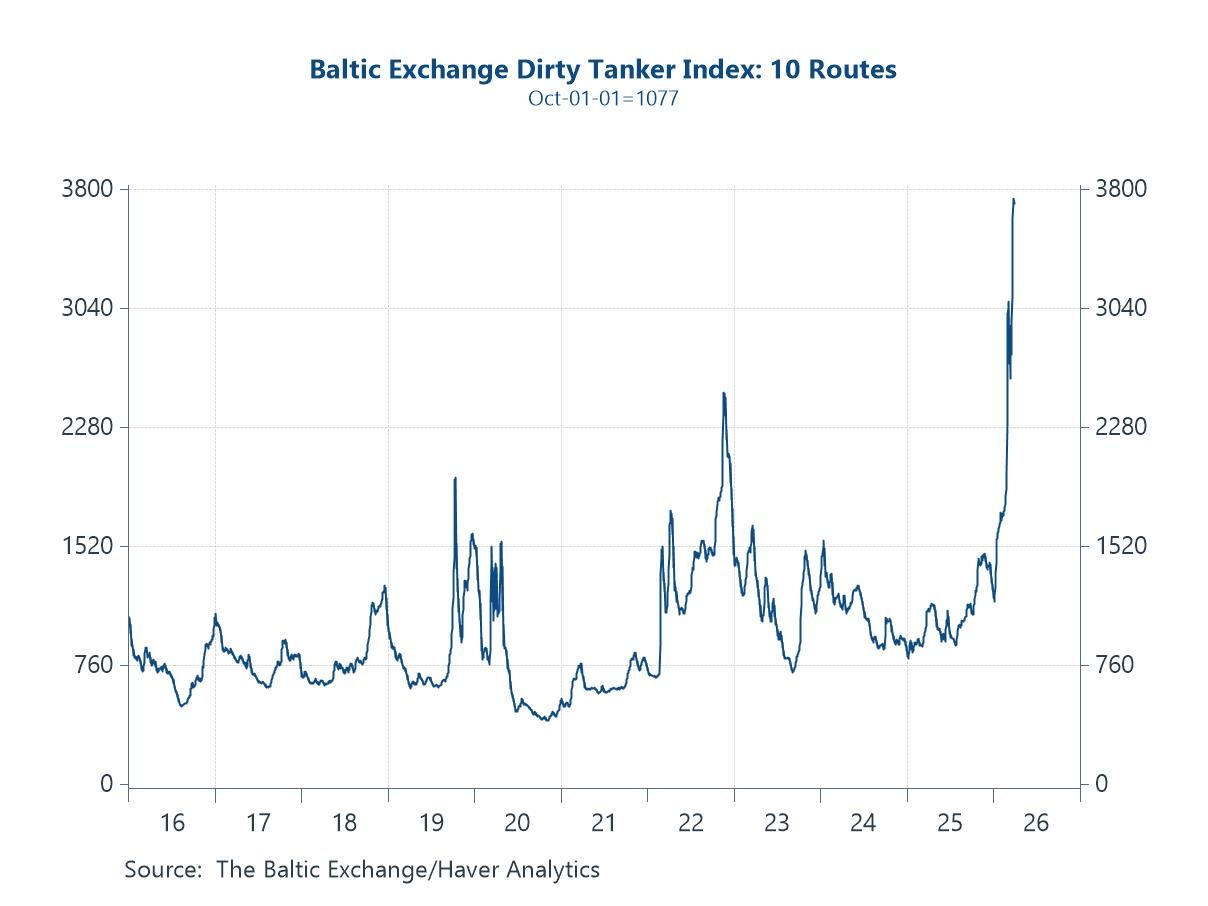

GlobalAmid tentative signs of de-escalation from the US administration over the past 48 hours—including suggestions that the conflict with Iran could conclude relatively quickly—financial markets have begun to retrace some of last week’s sharp repricing of Middle East risk. Oil prices have come off their highs, while equities and bonds have rallied as risk premia ease. That said, the earlier phase of the week saw a decisive adjustment: oil surged, front-end yields moved higher, and uncertainty rose as investors grappled with the implications of disrupted energy flows. Even now, the overall adjustment has been uneven—volatility has picked up, but not to levels typically associated with sustained geopolitical stress—raising questions about how fully markets are internalising both the risks and the rapidly shifting outlook. Our charts this week capture these cross-currents. Tanker rates have spiked as shipping routes are disrupted and capacity tightens (chart 1), while PMI delivery times point to early signs of supply chain strain feeding into the real economy (chart 2). At the same time, the divergence between elevated policy uncertainty and relatively contained market volatility suggests there could have been a degree of complacency (chart 3). The rise in oil prices is already feeding into higher short-term yields, though this is being tempered by cooling labour markets, anchored inflation expectations and more cautious central bank signalling (charts 4 and 5). Meanwhile, euro area flash CPI has picked up, but core inflation remains relatively benign, suggesting underlying price pressures are still contained for now (chart 6).

USA| Apr 01 2026

USA| Apr 01 2026U.S. Retail Sales Rebounded in February

- Total sales increased 0.6% m/m after a 0.1% m/m decline in January

- Excluding autos, sales increase 0.5% m/m in February after having been unchanged in January.

- Sales of the retail control group that is used to construct PCE rose 0.5% m/m in February.

by:Sandy Batten

|in:Economy in Brief

USA| Apr 01 2026

USA| Apr 01 2026U.S. ADP Private Employment Growth in March Above Forecasts

- Private payrolls +62K in March, ninth straight m/m gain.

- Hiring increase driven by small businesses (+85K), strongest since August.

- Service-sector jobs up (+32K), led by education & health svs. (+58K) and information (+16K), partly offset by trade, transp. & utilities (-58K).

- Goods-producing jobs up (+30K), driven by construction (+30K).

- Wage growth accelerates y/y for job changers (6.6%, a three-month high) but steady for job stayers (4.5%).

USA| Apr 01 2026

USA| Apr 01 2026U.S. Mortgage Applications Dropped in the March 27 Week

- Both applications for loans to purchase and for loan refinancing dropped in the latest week.

- Interest rate on 30-year fixed-rate loans rose 14bps to 6.76%

- Average loan size declined.

Europe| Apr 01 2026

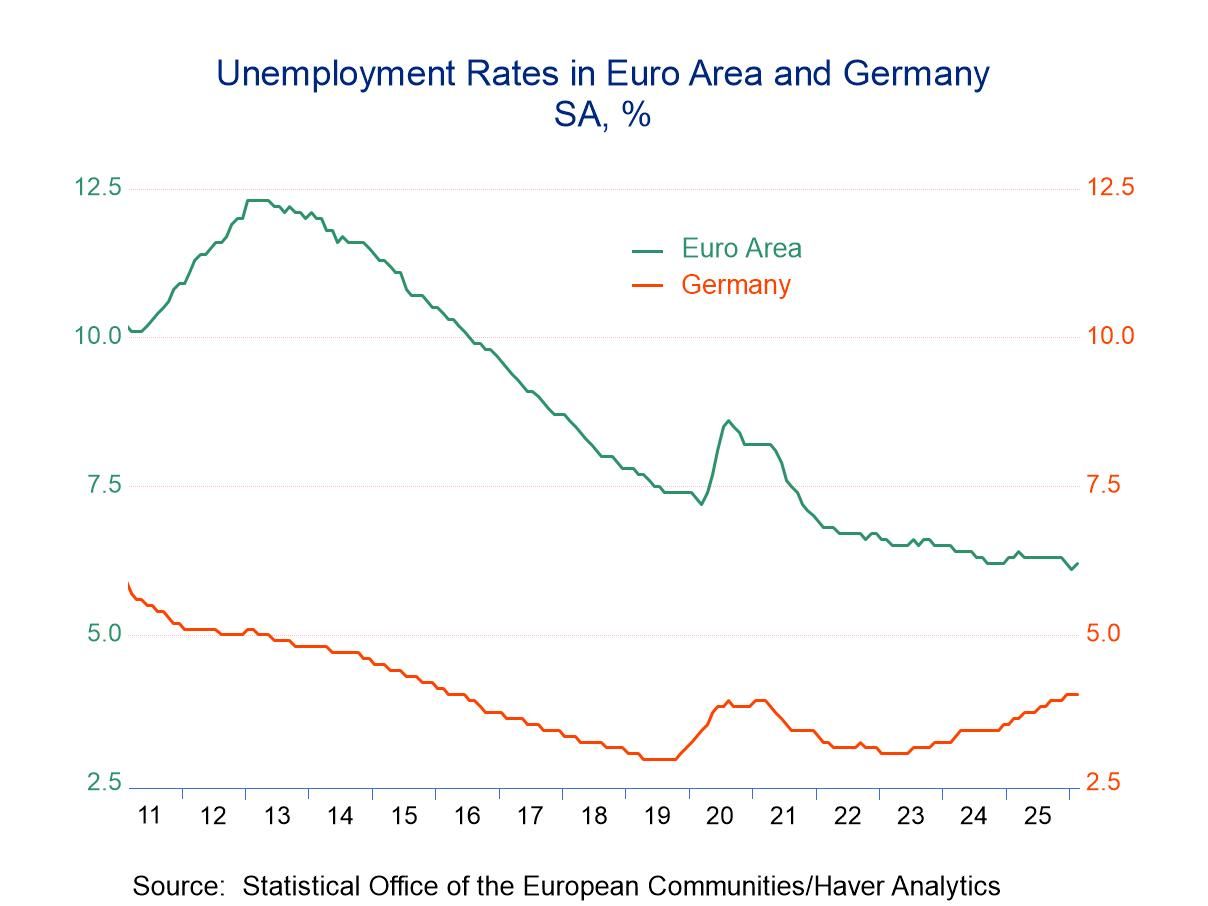

Europe| Apr 01 2026EMU Unemployment Rate Ticks Up; Still Near All-Time Low

The unemployment rate in the European monetary union picked up to 6.2% in February from 6.1% in January, when it had declined from 6.2% in December. The 6.1% reading is the all-time low, so at 6.2% the unemployment rate remains extremely low in the monetary union.

The number of unemployed in February rose by about 1% in both the EU and the monetary union; however, over broader spans of three months, six months, and 12 months, the number of unemployed is still falling.

February is a low month for the number of reporters on the table showing a decline in the unemployment rate. Among the 12 member reporters listed in the table, only Spain had a lower unemployment rate in February than in January, and Spain continues to show declines in unemployment as it also saw its unemployment rate drop in January and December, as well as on balance over three months, six months, and 12 months. Spain is the only country in the monetary union showing this kind of ongoing progress in reducing unemployment.

For the most part, unemployment rates seem to be stuck at relatively low levels among these 12 monetary union reporters. Four show net declines over 12 months, while six show declines over six months and four show declines over three months. Only three—Austria, Finland, and Luxembourg—report unemployment rates that rank above their respective medians, above a ranking of 50% on data back to 2000.

Although the EMU unemployment rate ticked up in February, it remains exceptionally low. Unemployment in Italy also ticked higher and has the exceptionally low ranking of 0.2%, having just moved up from its all-time low. Country-reported unemployment rates are in the bottom 10 percentile of their range over this period in Spain and Greece. You will remember these as the countries with the structurally highest unemployment rates typically in double digits prior to the formation of the European Union; now the Greek unemployment rate is 8.5% and the Spanish unemployment rate is 9.8%, and they are gradually folding into the community norms.

Despite the uptick in the unemployment rate, it's another excellent unemployment report for the monetary union, with unemployment rates below the medians up and down the line with few exceptions and with both countries brandishing unemployment rates that are substantially below their historic medians. Inflation rate in the monetary union remains broadly controlled, and the progress on the unemployment rate has been spectacular. Despite the other problems that the monetary union has encountered, these are true successes of the formation of the monetary union.

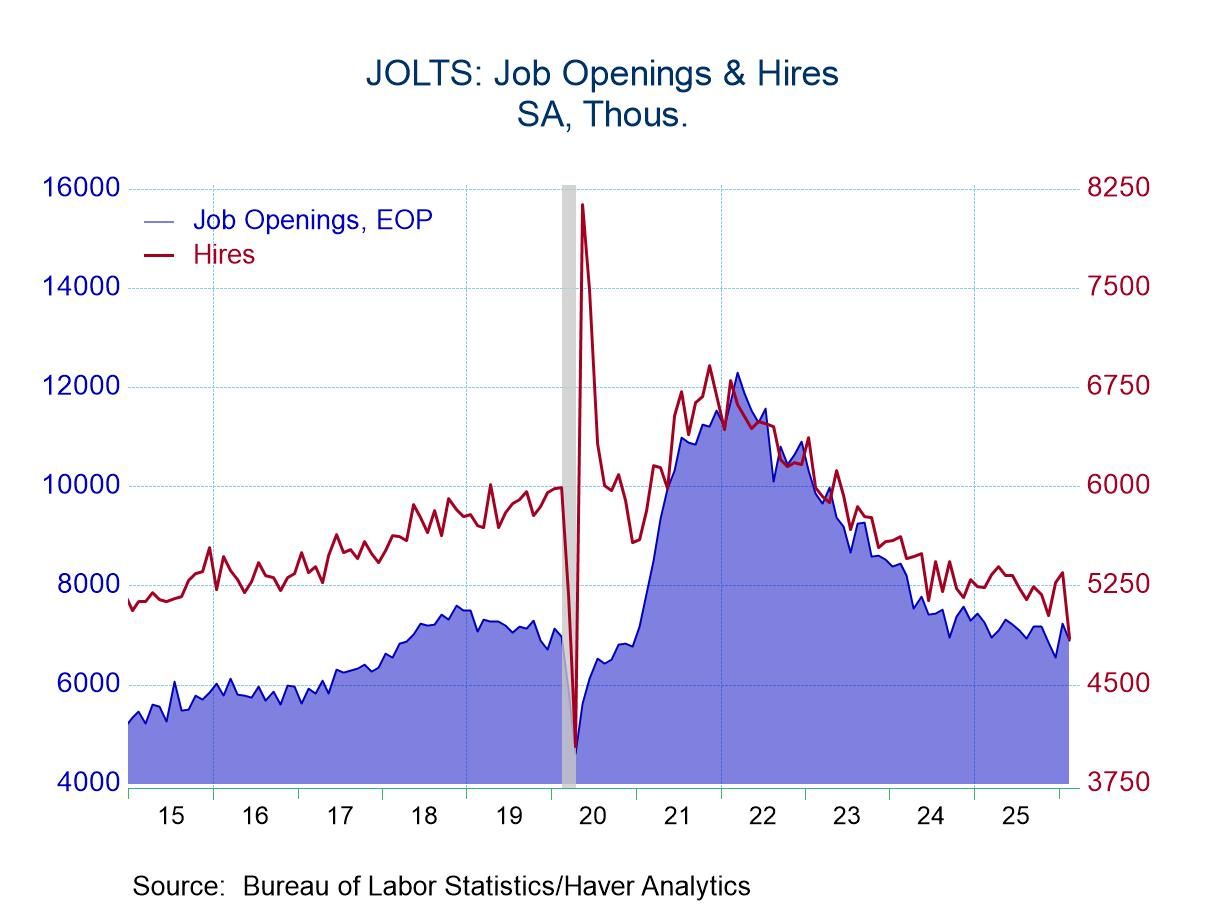

USA| Mar 31 2026

USA| Mar 31 2026U.S. JOLTS: Openings and Hiring Fell in February

- Openings fell 4.9% m/m to 6.882 million from an upwardly revised 7.240 million in January.

- Hiring plummeted 9.3% m/m to 4.849 million, the lowest reading since April 2020.

- Separations fell 3.4%% m/m to 4.971 million with a decline in Quits and an increase in Layoffs.

by:Sandy Batten

|in:Economy in Brief

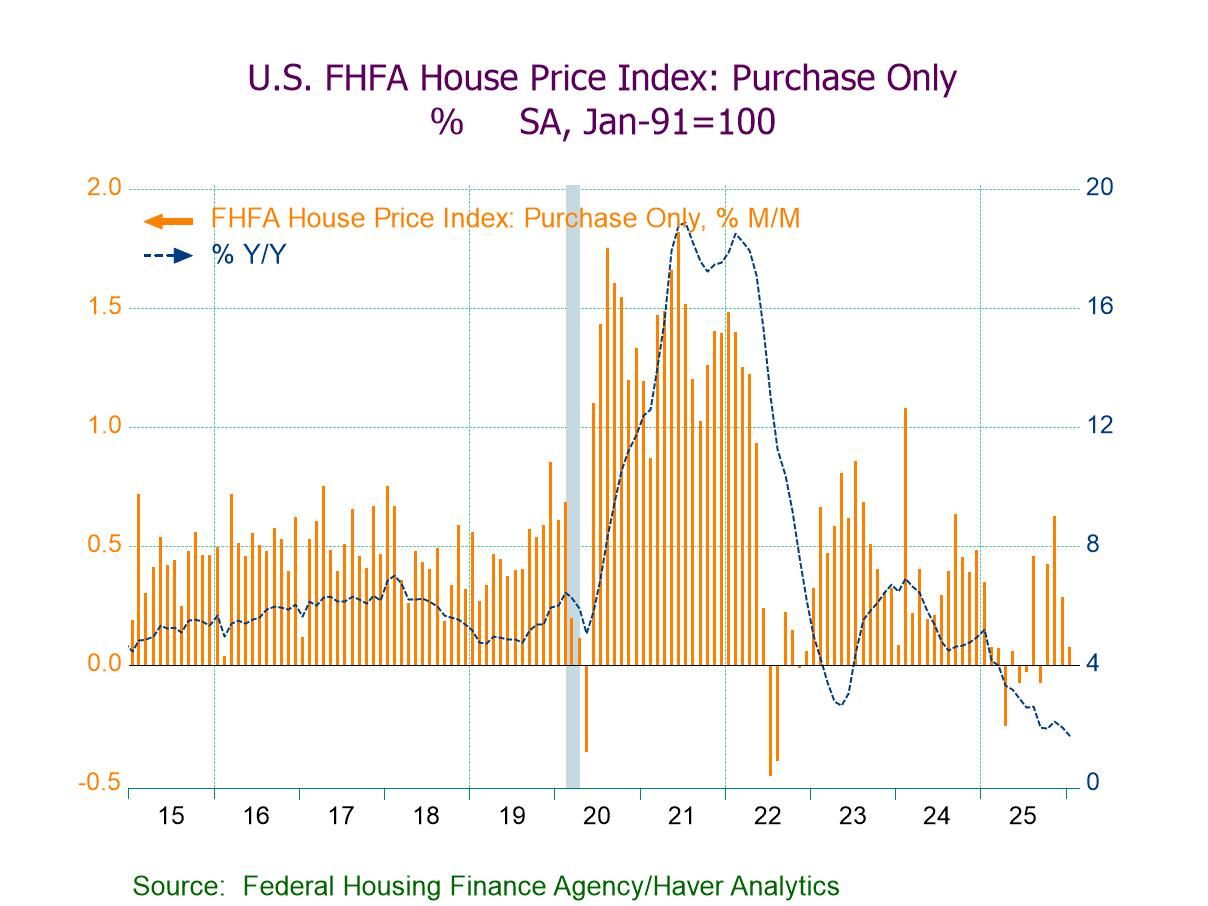

USA| Mar 31 2026

USA| Mar 31 2026U.S. FHFA House Price Growth Continues to Decelerate in January

- FHFA HPI +0.1% (+1.6% y/y) in Jan., the smallest of four straight m/m gains.

- House prices up m/m in six of nine census divisions, led by East South Central (+1.7%), but down in West South Central (-0.7%), South Atlantic (-0.4%), and East North Central (-0.1%).

- House prices up y/y in six of nine regions, led by East North Central (+4.4%), but down in West South Central (-0.8%) and Pacific (-0.5%).

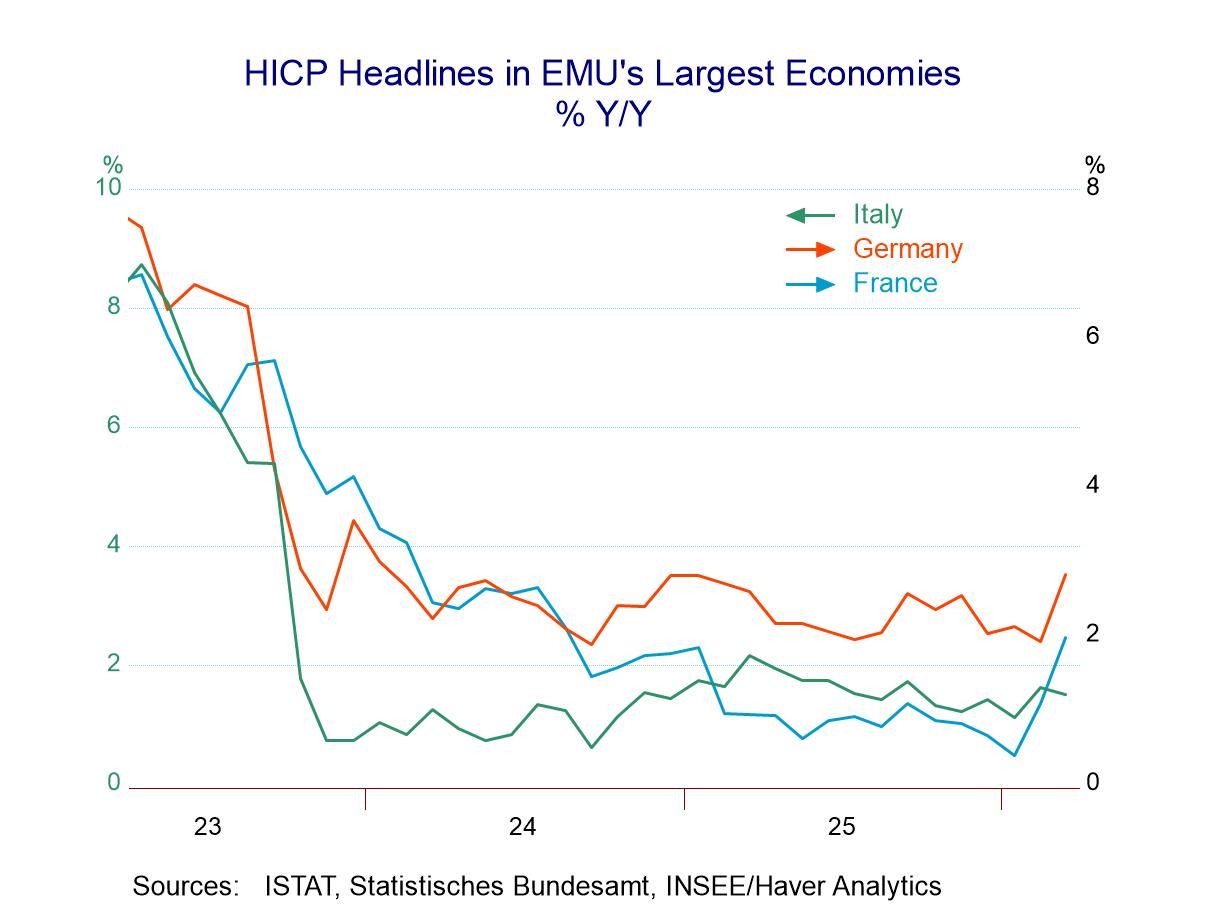

Europe| Mar 31 2026

Europe| Mar 31 2026EMU Inflation Surges; Core Clings to Old Trend

Inflation has begun to flash higher in the euro area as the early inflation indicators in March show an increase of 0.7% month-to-month, even as the core sticks to a low reading of 0.1% in March.

Large economy HICP headlines show pressure The month-to-month increases in the large economies and the monetary union are giving off uncomfortable readings, with Germany posting a 0.9% increase month-to-month, France 0.7%, Italy a more subdued 0.3%, and Spain 0.6%. These numbers help to produce excessive 3-month inflation rates of 4.4% annualized for Germany, 4.5% for France, 3.6% for Italy, and 2.7% for Spain—all of them over the top (that expression, of course, refers to European Central Bank’s inflation objective of 2%).

Year-on-year trends What I listed above are the three-month annualized inflation rates. What the ECB is more interested in is the more-subdued and better-behaved year-over-year rate. On that score, the year-over-year rate is 2.8% for Germany, 2% for France, 1.5% for Italy, and 3.2% for Spain. For the European Monetary Union as a whole, it is 2.5%, while for the EMU core, inflation is 2.2%.

In terms of the year-over-year inflation rates, Germany and Spain are clearly excessive. France is basically on the money for target, while Italian inflation is running cool. GDP-weighted inflation in the monetary union is too high at 2.5%, and on a core basis, it is at what is probably an acceptable 2.2% pace—above target but not demonstrably so.

Core inflation Core inflation or ex-energy inflation, for the three countries that report early show the ex-energy inflation rate for Germany at 2.3% over 12 months; in Italy it is 1.8%, and for Spain it is 2.7%. The core inflation rates are on the high side—not extraordinary, but nevertheless elevated—and the headline inflation rates themselves are accelerating. Looking at the 3-month, 6-month and 12-month inflation rates, we see acceleration in play for Germany, France, Italy, and Spain, as well as, for the monetary union as a whole where the 3-month inflation rate has reached 5% annualized (yikes!).

Oil…no! Don’t blame oil yet—that lies ahead We know that oil prices are spurting, but on this timeline ending in March, Brent oil prices measured in euros fell by 2.3%, and year-over-year Brent oil prices are down by 22.6%. So these results are yet to be clobbered by events in the Middle East—events that have lifted oil prices and other energy costs quite dramatically.

- of2736Go to 30 page